•

1 min read

Short-Term Investment Options in India for 1 to 90 Days

When you need your money back in a few days, a few weeks, or within 3 months, the usual investing advice stops being useful.

Most “short-term investment options in India” articles mix together products meant for 30 days with products meant for 3 to 5 years. That creates confusion. If your rent is due in 20 days, your credit card bill hits next month, or you are building a travel fund for the next 60 days, your priority is not chasing maximum returns. It is protecting capital, accessing money on time, and earning something better than idle cash where possible.

That is exactly how this guide is structured.

This article focuses only on true short-term investment options in India for 1 to 90 days. We will compare the most practical places to park idle cash: savings accounts, sweep FDs, liquid funds, overnight funds, Treasury Bills, and higher-yield spending-style setups. We will also look at which option fits real-life use cases like salary float, emergency cushions, near-term travel, and money waiting for bills.

If you are searching for the best short term investment for 1 month in India, wondering where to park money for 30 days in India, or looking for safe short term investment options in India, this guide will help you make a cleaner decision.

Why the 1–90 day window needs a different strategy

Money you need soon behaves differently from money meant for wealth creation.

For a 1–90 day time horizon, the main decision filters are:

Liquidity: How fast can you access the money?

Capital stability: Can the value fluctuate even a little?

Return expectation: Is the extra return meaningful after such a short holding period?

Ease of use: Can you move funds with minimal friction?

Purpose-fit: Is the product suitable for spending, parking, or locking till maturity?

That is why the best place to keep money for a few weeks is often not the same as the best place for 1 year.

If you are still holding all near-term money in a low-yield savings account, it helps to first understand the cost of idle cash and why so many savers are rethinking where they park short-duration money. See Why Most People Lose Money Without Realising It - The Hidden Cost of Idle Cash and How Much Money Are You Losing by Keeping ₹1 Lakh in a Savings Account?.

Quick comparison: short-term parking options for 1 to 90 days

Option | Best for | Time horizon | Liquidity | Capital risk | Return potential | Watch-outs |

|---|---|---|---|---|---|---|

Savings account | Bills, UPI, ATM usage, emergency access | 1–30 days | Instant | Very low | Low | Usually poor post-tax real return |

Sweep-in FD | Cash you may or may not use soon | 7–90 days | Usually good, bank-dependent | Low | Slightly better than savings in some cases | Terms vary by bank |

Overnight fund | Money parked for a few days to a couple of weeks | 2–30 days | High, but not instant like a bank account | Low, not zero | Slightly above savings in some periods | Mutual fund cut-off/NAV timing matters |

Liquid fund | Salary float, bill money, short-goal parking | 7–90 days | High | Low, not zero | Better than savings in many cases | Not a direct substitute for daily-spend cash |

Treasury Bills | Funds you can lock to maturity | 14–91 days and up | Tradable, but best held till maturity | Sovereign credit quality if held to maturity | Competitive for locked cash | Less convenient for day-to-day access |

Higher-yield spending setup | Spending money you want to keep productive till use | 7–60 days | Designed for spend access | Structure-dependent | Better utility than idle savings for some users | Understand how access and withdrawals work |

Simple rule: for this time horizon, convenience and timing often matter more than a tiny return difference.

1. Savings account: best for money you may need today

For money you might need within hours, a savings account remains the default choice.

This is still the right home for:

rent due this week

ATM cash needs

UPI transactions

emergency access buffer

money you cannot afford to delay by even a day

The problem is not safety or convenience. The problem is yield. If large chunks of money sit there for weeks with no immediate use, they often underperform inflation and create a silent drag on your finances.

Best use case

Use a savings account for:

0 to 7 days of spending cash

emergency access money

amounts that must remain fully transaction-ready

Not ideal for

salary money sitting idle for 2 to 8 weeks

travel funds you will use next month

money waiting for EMI or card payment after payday

For a deeper side-by-side look, read Savings Account vs Liquid Fund vs HYSA in India 2026: A Side-by-Side Comparison for Working Professionals.

2. Sweep-in fixed deposits: good if your bank offers flexible auto-parking

A sweep-in FD links your savings account with a fixed deposit. Surplus money above a threshold can move into an FD, while withdrawals can trigger reverse sweep features depending on your bank.

This can work if you want:

a familiar bank-led experience

some automation

better yield than a plain savings account

no need to open a separate investment app

Pros

easy for conservative users

often better than leaving all funds in savings

can suit money that may or may not be used over the next 1 to 3 months

Cons

flexibility differs from bank to bank

premature breakage rules vary

not always ideal for multiple short, uneven withdrawals

Best use case

Good for people who want a bank-native answer to “where to park money for 30 days in India” and value familiarity over optimization.

Verdict

Convenient, but not always the smartest option if you are comparing all investment options for idle cash in India.

3. Overnight funds: useful for ultra-short holding periods

If your holding period is very short, overnight funds deserve more attention than they usually get.

An overnight fund invests in securities with a 1-day maturity profile, which reduces interest-rate sensitivity compared with longer-duration debt funds. SEBI’s mutual fund framework distinguishes overnight funds and liquid funds as separate short-duration categories, and liquid/overnight funds are subject to specific risk-management norms. (sebi.gov.in)

Why they matter

For money that is idle for:

a few days

1 week

maybe 2 to 3 weeks

overnight funds can be a cleaner fit than products built for longer holding periods.

Pros

lower duration risk than many other debt categories

suitable for very short parking

potentially modest improvement over idle savings, depending on rate conditions

Cons

still a mutual fund, so it is not a bank account

purchase/redemption timing matters because mutual fund cut-off rules affect applicable NAV. AMFI publishes cut-off timing guidance for subscriptions and redemptions. (amfiindia.com)

returns are not guaranteed

Best use case

Money you want to park for a few days to a couple of weeks without trying to stretch for yield.

Verdict

Among the safest short term investment options in India for very short windows, overnight funds are worth considering if you are comfortable using mutual funds.

4. Liquid funds: one of the best options for 7 to 90 days

If you ask experienced savers where to park short-duration money that is not needed instantly, liquid funds come up again and again.

That is because liquid funds are designed for short-term cash management, not long-term compounding. They are commonly used for salary float, emergency buffers, bill money, and near-term goals.

SEBI defines liquid funds as open-ended debt schemes investing in debt and money market instruments with maturity of up to 91 days. (sebi.gov.in)

Why liquid funds work for this window

They strike a useful balance between:

relatively high liquidity

low duration profile

better parking efficiency than leaving money idle

easier access than locking money into many traditional options

Best use cases

Liquid funds are especially practical for:

salary credited today, expenses due over the next 2 to 6 weeks

travel money for the next month or two

credit card due amount waiting for payment date

a layer of emergency fund not needed instantly

freelancers smoothing irregular cash flow

Important caution

A liquid fund is not exactly like a bank account. Access is fast, but not “swipe now, settle later” fast in the way a savings account is. Mutual fund processing, cut-off, and withdrawal timelines matter. AMFI publishes general cut-off timing rules, and practical access can depend on redemption timing and the platform you use. (amfiindia.com)

If you want to understand this in plain English, these guides help:

Verdict

For many people looking for the best short term investment for 1 month in India, liquid funds are among the strongest options.

5. Treasury Bills: strong for locked money, weaker for flexible spending cash

Treasury Bills, or T-bills, are short-term government securities issued at a discount and redeemed at face value on maturity. The RBI notes that T-bills are issued regularly, and retail investors can access government securities through the RBI Retail Direct platform. (rbi.org.in)

Why T-bills are interesting

If you know with confidence that you do not need the money until maturity, T-bills can be appealing because they offer:

sovereign backing

defined maturity

simple return math if held till maturity

Why they are not perfect for everyone

For money needed in the next few weeks, T-bills are often less convenient than liquid funds or bank-linked options because:

they are better suited to planned holding periods

convenience is lower for frequent movement

they are not designed for everyday cash management

Best use case

A good fit when you know:

exact date of need

exact amount

no need for intermediate withdrawals

Verdict

Excellent for disciplined short locking. Less ideal as a flexible answer to “best place to keep money for a few weeks.”

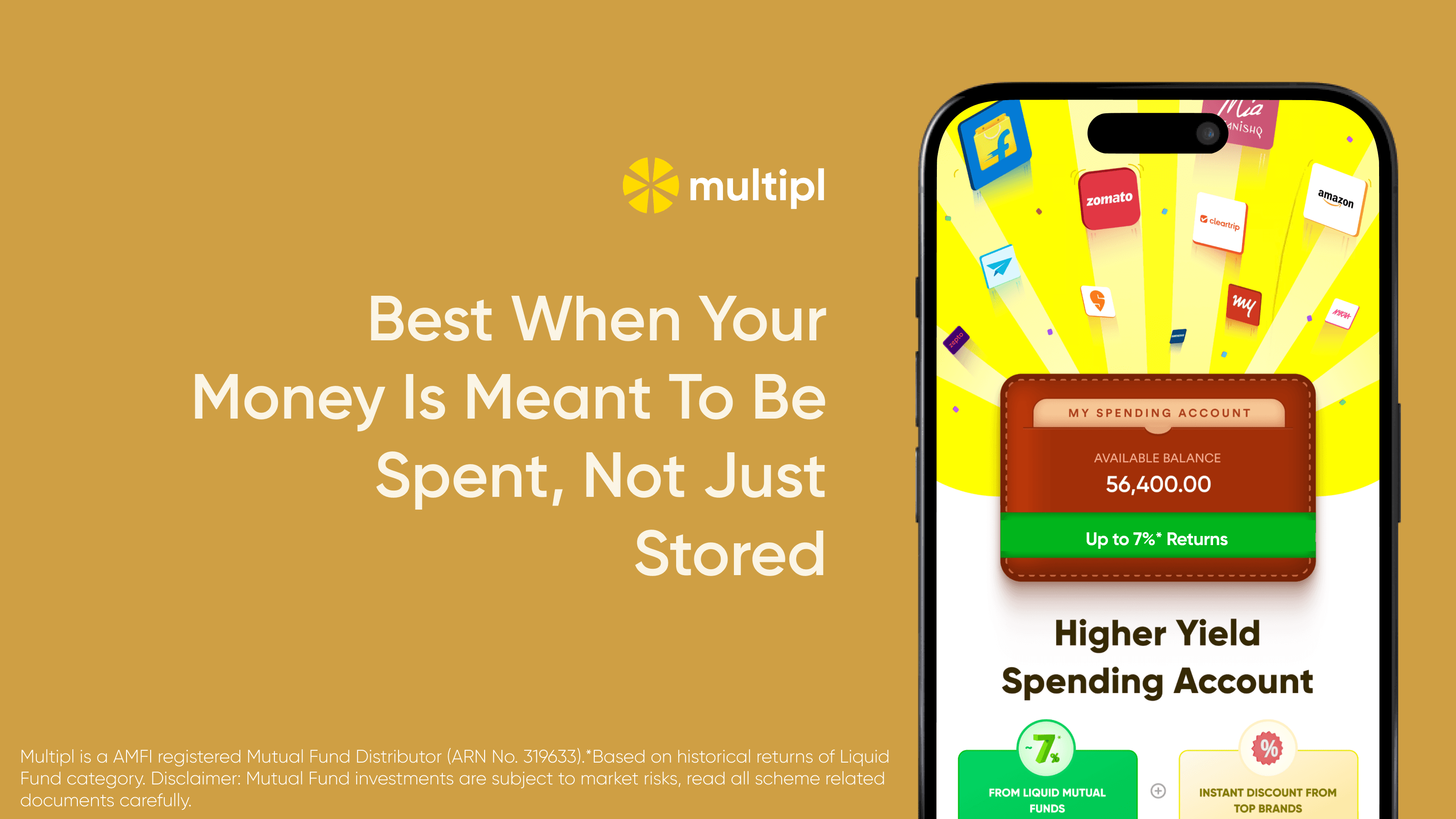

6. Higher-yield spending-style setups: best when your money is meant to be spent, not just stored

A lot of short-term money in real life is not “investment money.” It is future spending money.

That includes:

travel budgets

shopping money

festival spending

planned lifestyle expenses

salary cash that will get used over the month

This is where a higher-yield spending-style setup can stand out. Instead of keeping all future spending in a low-yield account, some users prefer a system where money remains more productive until they actually spend it.

If that idea is new to you, start with What Is a Higher-Yield Spending Account (HYSA) and How Does Multipl Work? A Complete 2026 Guide and The Spending Money Hack: How to Use HYSA to Earn While You Shop.

Best use case

This works well for:

planned discretionary spending

monthly spend buckets

short-term goals where you want access plus better money behavior

Verdict

For people asking, “Can I use a liquid fund like a bank account in India?”, the practical answer is usually: not exactly. A purpose-built spending setup may feel closer to that experience than a plain investment app.

How to choose the right option by purpose

Here is the simplest decision framework.

If you need the money in 1 to 7 days

Choose:

Savings account

Overnight fund, only if you understand fund timing and do not need instant spend access

If you need the money in 7 to 30 days

Choose:

Liquid fund

Sweep FD

Higher-yield spending setup, if the money is meant for planned spending

If you need the money in 30 to 90 days

Choose:

Liquid fund

T-bill, if you can lock till maturity

Sweep FD, if you prefer a bank route

For a broader decision tree, read The Complete Guide to Managing Short-Term Money in India (2026) and Short-Term Investment Options in India: 8 Safe Places for Idle Money.

A practical framework for salaried professionals

If you are salaried, your money does not arrive and leave on the same day. That creates a “salary float” period.

A useful way to split it:

Instant-access money: 5 to 10 days of expenses in savings

Near-term monthly obligations: money for cards, rent, EMIs, travel, or planned spending parked more efficiently

Emergency layer: one part instant, one part slightly higher-yield but still liquid

This is where liquid funds often become especially relevant. For more on that, see Salary in Liquid Fund: How Much Should You Keep? and Where Should Salaried Indians Keep Money Between Payday and Bill Day?.

Common mistakes to avoid with 1–90 day money

1. Chasing the highest headline return

For very short periods, return differences may be small in rupee terms. A delay in access can matter more.

2. Treating all debt products as equally safe

Even low-risk options have different structures. Understand whether you are using a bank deposit, mutual fund, or government security.

3. Parking bill money in something you do not fully understand

If you need the money for a due date, choose simplicity over cleverness.

4. Locking flexible cash unnecessarily

If the amount may be needed any day, avoid over-optimizing.

5. Ignoring the use-case

The best answer depends on whether the money is for:

emergency access

salary float

near-term planned spending

locked short-duration parking

So, what is the best short-term investment option in India for 1 to 90 days?

Here is the clean verdict:

Best for same-day access: Savings account

Best for a few days: Overnight fund

Best for 1 to 3 months of idle cash: Liquid fund

Best for conservative bank users: Sweep FD

Best for fixed holding till maturity: Treasury Bills

Best for planned spending money: Higher-yield spending-style setup

If your main goal is simply to stop losing money on idle cash while keeping access reasonably smooth, liquid-fund-based setups and smarter spend-management flows often outperform the old habit of leaving everything in savings.

If you want to compare app-based options specifically, check Liquid Fund Apps in India: Compare Liquidity, Returns and Minimums and explore the broader Multipl blog for more guides on idle cash, liquid funds, and smarter short-term money management.

Conclusion

The best short-term investment options in India are not about maximizing return at all costs. They are about matching the product to the timeline and purpose of the money.

For 1 to 90 days, ask three questions:

When exactly will I need this money?

Do I need instant spending access or just fast withdrawal?

Am I parking cash, or am I preparing to spend it?

Once you answer those, the choice becomes much simpler.

For most people:

keep immediate-use cash in savings,

consider overnight funds for ultra-short parking,

use liquid funds for 1 to 90 day idle cash,

and use purpose-based spend systems when the money is meant to be used soon anyway.

That is a more realistic way to handle near-term money than treating every rupee as either “invested for years” or “stuck in savings forever.”

FAQs

What is the best short term investment for 1 month in India?

For many people, liquid funds are one of the best options for a 1-month horizon because they are designed for short-term cash parking. If you need instant transaction access, a savings account may still be better.

Where should I park money for 30 days in India?

The answer depends on access needs. For spending and bill money, savings or a spending-linked setup may work best. For idle cash not needed instantly, liquid funds are often a strong fit. If you want a bank-led approach, consider a sweep FD.

Are liquid funds safe for parking idle cash in India?

Liquid funds are generally considered low-risk short-duration debt funds, but they are not risk-free and not the same as bank deposits. They can suit short-term parking if you understand liquidity timelines and product structure.

Can I use a liquid fund like a bank account in India?

Not exactly. A liquid fund can help you park money efficiently, but it does not function like a normal day-to-day bank account for UPI, ATM, or instant merchant use.

What is the best place to keep money for a few weeks?

For a few weeks, the best place depends on purpose: savings for immediate access, overnight funds for very short parking, liquid funds for short idle cash, and T-bills only if you can lock the money to maturity.

What are safe short term investment options in India for 1 to 90 days?

The most practical options are savings accounts, sweep FDs, overnight funds, liquid funds, and Treasury Bills. The safest choice for you depends on whether you need instant access, flexible withdrawal, or a fixed maturity date.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633).

*Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.