•

1 min read

Savings Account vs Liquid Fund vs HYSA in India 2026: A Side-by-Side Comparison for Working Professionals

Excerpt:

Three products can hold your idle money today: savings accounts, liquid mutual funds, and Higher-Yield Spending Accounts (HYSA). Each works differently. This 2026 comparison breaks down all three across eight dimensions so you can decide whether moving money out of a traditional savings account actually makes sense.

Why This Comparison Matters in 2026

For decades, the default place to keep money in India has been a savings account.

It’s familiar.

It’s simple.

And it’s instantly accessible.

But financial products have evolved. Today, many working professionals compare savings accounts with liquid mutual funds and newer fintech products such as Higher-Yield Spending Accounts (HYSA).

The reason is simple: idle money often sits unused for days or weeks before being spent.

Where that money waits can affect how efficiently it works.

Before deciding what to do with idle money, it helps to understand how these three options differ.

What Is a Savings Account?

A savings account is the most common place to store cash.

Banks design savings accounts primarily for:

• deposits

• withdrawals

• daily transactions

• UPI payments

Interest rates on savings accounts in India typically range around 2.5% annually, depending on the bank.

Key Characteristics

• Instant liquidity

• Bank-determined interest rates

• Deposit insurance up to ₹5 lakh (DICGC)

Savings accounts are optimized for convenience and safety, not necessarily for maximizing short-term returns.

What Is a Liquid Mutual Fund?

A liquid mutual fund is a debt mutual fund that invests in very short-term money market instruments.

Under SEBI regulations, these instruments have maturities of up to 91 days.

Common holdings include:

• Treasury Bills

• Commercial Papers

• Certificates of Deposit

• Short-term government securities

Because these instruments mature quickly, liquid funds tend to show low volatility compared to longer-duration debt funds.

Historically, liquid funds have often generated higher yields than savings accounts, though returns vary with market conditions.

What Is a Higher-Yield Spending Account (HYSA) in India?

A Higher-Yield Spending Account (HYSA) is a fintech structure designed to help users manage money that will eventually be spent.

Instead of keeping spending money idle in a savings account, funds are typically allocated to short-term instruments such as liquid mutual funds, allowing the money to remain productive while waiting to be used.

Key characteristics:

• Potential yields linked to liquid fund returns

• High liquidity

• No lock-in period

• Often integrated with spending platforms

The idea is simple: spending money can earn returns until the moment it is used.

Savings Account vs Liquid Fund vs HYSA: Full Comparison

Below is a side-by-side comparison across eight important dimensions.

Feature | Savings Account | Liquid Mutual Fund | Higher Yield Spending Account |

Returns | ~2.5%–4% annually | Historically ~7% depending on market | Linked to liquid fund returns |

Liquidity | Instant withdrawal | T+1 redemption (some instant options) | Instant / quick redemption |

Lock-in | None | None | None |

Risk | Bank counterparty risk | Low market risk | Same underlying as liquid funds |

Taxation | Taxed as income | Debt fund taxation rules | Same as underlying funds |

Minimum Amount | Usually none | Often ₹100–₹500 | Platform dependent |

Best For | Daily transactions | Parking idle cash | Spending money that sits idle |

Typical Platforms | Banks | Mutual fund platforms | Fintech spending platforms |

Is It Worth Moving Money Out of a Savings Account?

The answer depends on how the money will be used.

Savings accounts remain essential for daily transactions and payments.

However, many professionals notice that larger balances often sit idle for weeks.

For example:

• salary received on the 1st

• EMI paid on the 5th

• expenses spread across the month

During that time, a portion of money may remain unused.

Short-term parking options such as liquid funds or Higher Yield Spending Account structure is designed to make that idle window more efficient.

Which Is Better: Liquid Fund or Savings Account?

Liquid funds and savings accounts serve slightly different purposes.

Savings accounts are ideal for:

• salary deposits

• ATM withdrawals

• daily spending

Liquid funds are often used for:

• parking idle balances

• emergency funds

• short-term liquidity management

The key difference lies in how the money is utilized while waiting.

Savings accounts prioritize convenience.

Liquid funds prioritize short-term cash efficiency.

Best Apps to Manage Idle Money in India

Several platforms help users access liquid funds or related structures easily.

Here are five widely used apps.

1. Multipl

Multipl focuses on managing money that will eventually be spent.

Its Higher-Yield Spending Account allows funds to be linked to liquid mutual funds, helping idle spending money remain productive while waiting to be used.

Features include:

• quick redemption

• brand discount integrations

• spending-focused design

2. Groww

Groww is one of India’s most widely used investment apps.

Users can invest in liquid mutual funds directly through the platform.

Best for: beginners exploring mutual funds.

3. Zerodha Coin

Coin provides access to direct mutual funds, which typically have lower expense ratios.

Best for: investors who prefer direct plans.

4. ET Money

ET Money combines expense tracking with mutual fund investing.

Best for: people who want financial tracking and investments in one place.

5. Kuvera

Kuvera focuses on direct mutual fund investing and portfolio analysis.

Best for: experienced investors managing larger portfolios.

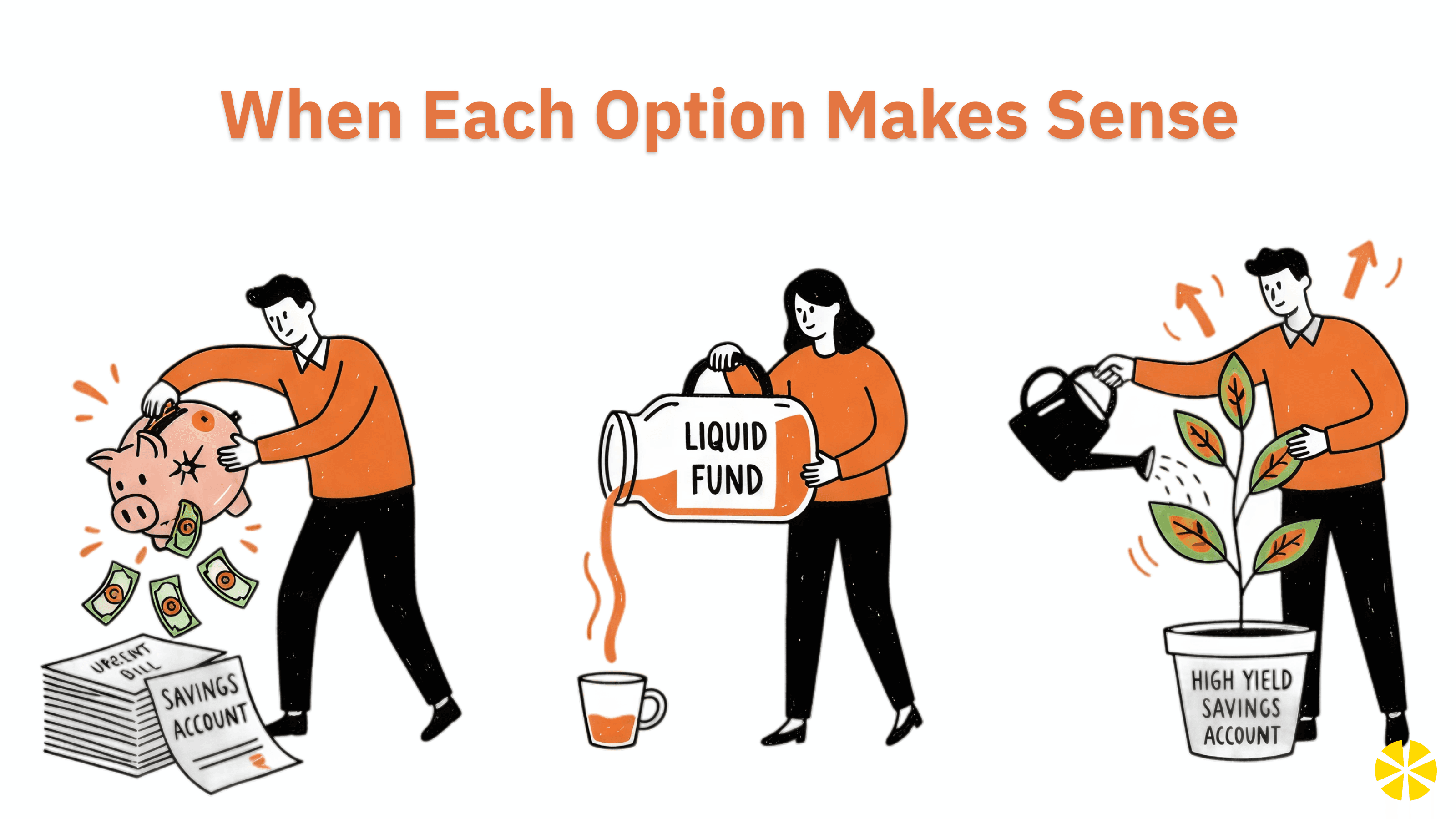

When Each Option Makes Sense

A simple framework can help you decide.

Use a savings account for

• daily payments

• ATM withdrawals

• salary deposits

Use liquid funds for

• emergency funds

• temporary idle balances

• short-term cash parking

Use HYSA structures for

• spending money waiting to be used

• short-term liquidity before purchases

FAQ

Is it worth moving money out of a savings account?

If a large balance sits unused for long periods, some investors move that portion into short-term instruments like liquid mutual funds or HYSA-style accounts while keeping transactional money in savings accounts.

What is a HYSA in India?

A Higher-Yield Spending Account (HYSA) is a structure offered by some fintech platforms where idle spending money is linked to short-term instruments such as liquid mutual funds.

Which is safer: savings account or liquid fund?

Savings accounts carry bank counterparty risk but offer deposit insurance up to ₹5 lakh. Liquid funds carry low market risk because they invest in short-term instruments, though they are still market-linked investments.

Which is the best alternative to a savings account for short-term money?

Many investors consider liquid mutual funds or fintech platforms offering HYSA-style accounts when managing idle balances that are not needed immediately.

Final Thought

Savings accounts remain the backbone of everyday banking.

But when it comes to idle money, the real question is not where your money starts.

It’s where it waits.

And understanding the difference between savings accounts, liquid funds, and newer HYSA structures can help working professionals make better short-term money decisions.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633). *Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.