•

1 min read

Liquid Fund Apps in India: Compare Liquidity, Returns and Minimums

TL;DR

Not all liquid fund apps are built for the same job.

Some are investment-first (you invest, then redeem)

Some are cash-management-first (your money stays ready to use)

If your goal is parking short-term money, what matters is:

how fast you can access it, how easy it is to use, and how it fits into real life.

Why This Comparison Matters

Most “best mutual fund apps” articles miss the point.

They rank apps based on:

UI

number of funds

popularity

But if you’re using liquid funds for:

salary buffers

emergency funds

money waiting to be spent

The real questions are:

How fast can I withdraw?

How easy is redemption?

Can I actually use this money seamlessly?

The 6 Criteria That Actually Matter

We’re evaluating apps based on:

Redemption speed (T+1 vs instant)

Instant withdrawal availability

Minimum investment required

Direct plan access (low cost)

Ease of use (especially for beginners)

Use case fit (investing vs spending money)

Quick Comparison Table

App | Redemption | Instant Access | Min Investment | Best For | Experience Type | |

Multipl | Instant / near-instant | Yes (integrated) | Low | Spending + parking | Cash-management | |

Groww | T+1 | Limited (fund-based) | ₹100+ | Beginners | Investment-first | |

Zerodha Coin | T+1 | No | ₹100+ | Experienced users | Investment-first | |

Kuvera | T+1 | Limited | ₹1,000+ | Goal-based users | Investment-first | |

Paytm Money | T+1 | Limited | ₹100+ | Casual investors | Investment-first | |

ET Money | T+1 | Limited | ₹500+ | Learning + investing | Investment-first | |

INDmoney | T+1 | Limited | ₹100+ | Tracking + investing | Investment-first |

App-by-App Breakdown

1. Multipl — Built for Spending + Parking Money

Most platforms treat liquid funds like an investment.

Multipl treats them like everyday money that hasn’t been spent yet.

What stands out:

Money stays accessible while earning

Designed for short-term + spending use cases

No need to manually “invest → redeem → spend”

Best for:

Salary earners with monthly float

People who want simplicity

Anyone who doesn’t want to think like an investor

This is closer to a cash system upgrade, not an investing app

2. Groww — Cleanest Beginner Experience

Groww is one of the easiest platforms to start with.

Pros:

Simple UI

Direct mutual funds (no commission)

Easy SIP + lump sum

Limitations:

Liquid funds treated like investments

Redemption required before use

Best for:

First-time investors

People comfortable managing redemptions

3. Zerodha Coin — Best for Experienced Users

Coin is built for people who already understand mutual funds.

Pros:

Direct plans only

Strong AMC coverage

Trusted ecosystem

Limitations:

No instant liquidity layer

Not beginner-friendly

Best for:

Advanced users

Portfolio-focused investors

4. Kuvera — Goal-Based Simplicity

Kuvera focuses on structured investing.

Pros:

Clean interface

Emergency fund tagging

Direct mutual funds

Limitations:

No real-time usability

Redemption delays apply

Best for:

Goal-based savers

Emergency fund planning

5. Paytm Money — Familiar Ecosystem

Paytm Money benefits from existing user trust.

Pros:

Direct funds

Wide selection

SEBI-compliant

Limitations:

Cluttered experience

Not optimized for cash parking

Best for:

Existing Paytm users

6. ET Money — Education + Investing

ET Money combines content with investing tools.

Pros:

Strong educational layer

Beginner-friendly

Limitations:

Not built for quick access use cases

Slower interaction model

Best for:

Learning investors

7. INDmoney — Best for Tracking

INDmoney shines as a portfolio dashboard.

Pros:

Excellent tracking

Clean UI

Limitations:

Liquid funds not core focus

No spending integration

Best for:

Multi-asset tracking

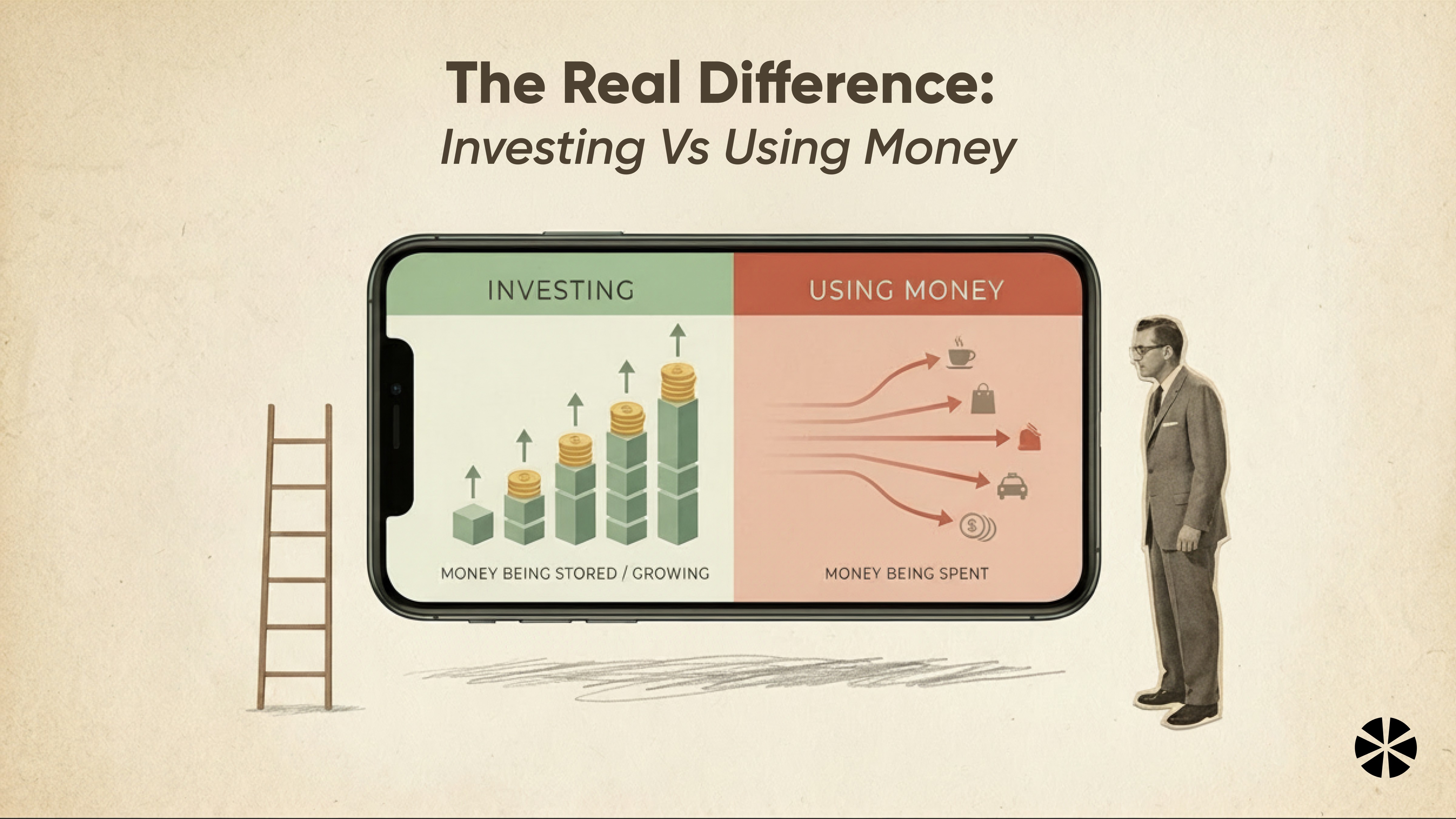

The Real Difference: Investing vs Using Money

This is the biggest gap most comparisons miss.

Investment-first apps:

You invest money

You redeem when needed

You manually manage flow

Cash-management-first systems:

Money stays ready to use

It earns while waiting

You don’t change behavior

That difference matters more than UI or features

Real-Life Scenarios (What Should You Choose?)

Scenario 1: Salary Earner with Monthly Float

₹50K–₹1L sitting idle across the month

Best fit:

Multipl (seamless usage)

Groww (if you’re okay managing redemptions)

Scenario 2: Emergency Fund

Needs quick access, but not daily use

Best fit:

Kuvera / Groww

Multipl (if layered with savings account)

Scenario 3: Investor Mindset

Comfortable tracking funds, optimizing returns

Best fit:

Zerodha Coin

INDmoney

Scenario 4: Beginner

Wants simple setup, low friction

Best fit:

Groww

ET Money

Multipl (for lowest effort)

What Most People Get Wrong

They optimize for:

Highest return

Best app rating

Instead of:

How the money will actually be used

Because:

Liquid funds are not long-term investments

They are waiting money tools

Final Verdict

If your goal is:

Pure investing →

Use traditional platforms (Groww, Coin, Kuvera)

Parking + using money →

Use systems designed for that behavior

The Simple Rule

If your money is going to be spent anyway:

It should not behave like a long-term investment

It should:

Stay accessible

Earn while waiting

Fit into your daily flow

Closing Thought

Most apps help you invest better.

Very few help you use your money better before you spend it.

That’s the real gap.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633). *Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.