•

1 min read

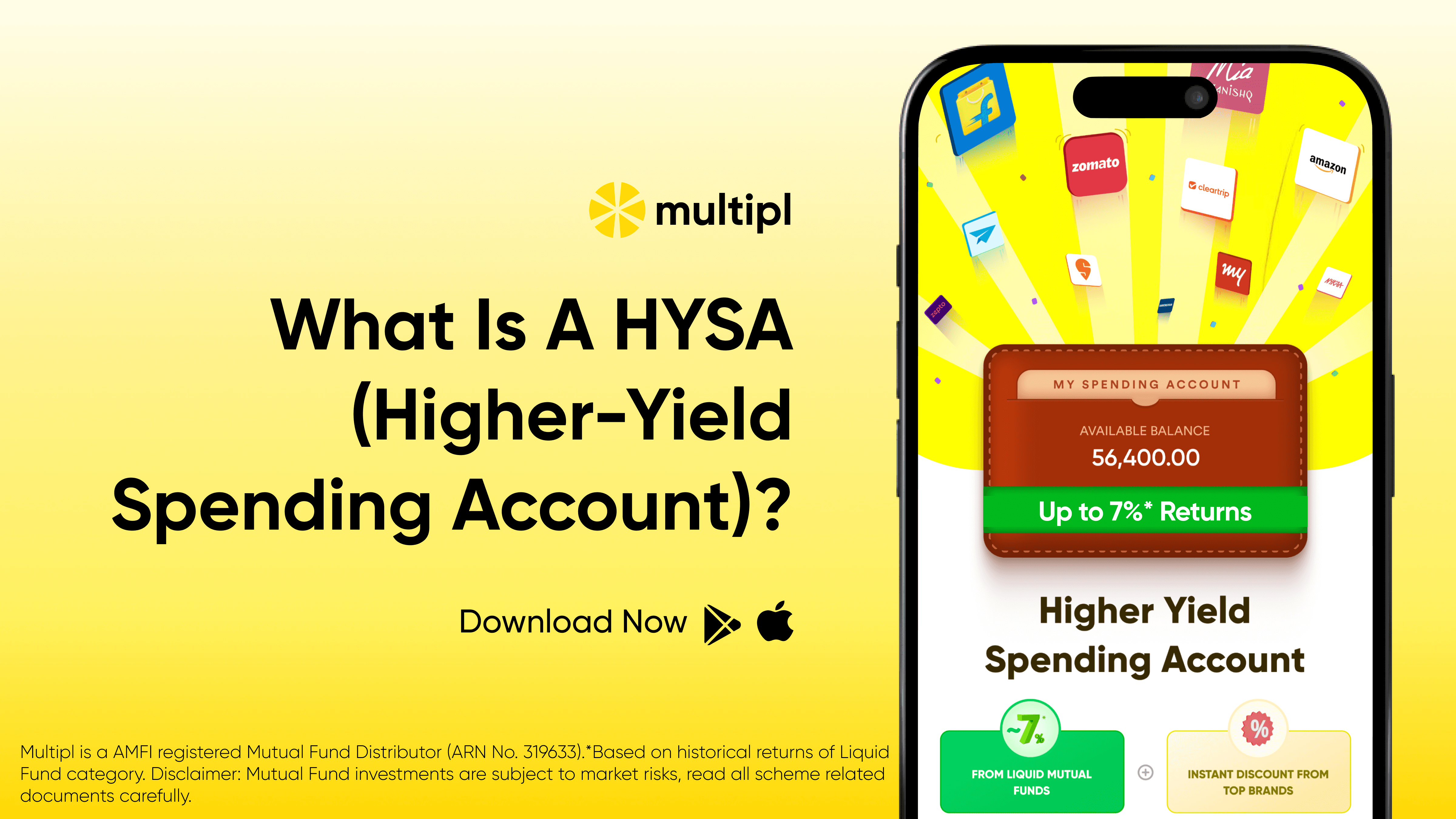

What Is a Higher-Yield Spending Account (HYSA) and How Does Multipl Work? A Complete 2026 Guide

TL;DR

A Higher-Yield Spending Account (HYSA) is a way to keep short-term spending money productive instead of leaving it idle in a regular savings account. In India, this usually means money is allocated to liquid mutual funds, which invest in very short-duration money market instruments and aim to offer better return potential than many standard savings accounts, while still keeping funds accessible. Multipl positions this as a spending-focused layer on top of liquid funds, helping users earn on idle cash, stay liquid, and withdraw or spend when needed.

HYSA is best suited for:

monthly salary balances that wait to be spent

upcoming bills, travel, shopping, and planned expenses

users who want better use of idle cash without a lock-in

> Important: HYSA returns are market-linked, not fixed like bank deposit interest, and liquid fund performance can vary.

Introduction

For decades, the default place to keep everyday money in India has been the savings account. Salary arrives. Bills get paid. Groceries, travel, and shopping happen across the month.

But most people miss one detail: their spending money often sits idle for days or weeks before they actually use it.

Traditionally, that idle money earns around 2.5% to 4% a year in many savings accounts, while liquid mutual funds have historically offered higher return potential, though returns are not guaranteed. In India, Multipl introduced the Higher-Yield Spending Account (HYSA) concept by combining liquid mutual funds with a spending interface built for everyday money.

This guide explains:

what a HYSA is

how Multipl works

how it compares with savings accounts

when it makes sense to use one

The Problem HYSA Solves

Think about a typical salary cycle.

Timeline | What Happens |

Day 1 | Salary credited |

Day 5 | EMI / rent payments |

Day 6–30 | Groceries, fuel, shopping, travel |

Between these events, a large portion of money waits before it is spent.

For many professionals, this idle window lasts 10–25 days every month. During that time, the money usually sits in a savings account earning relatively low interest.

HYSA is built for this gap.

What if spending money could earn returns until the moment it is used?

What Is a Higher-Yield Spending Account in India?

A Higher-Yield Spending Account (HYSA) is built to manage short-term idle money that will eventually be spent.

Instead of keeping that money entirely in a savings account, the funds are typically allocated to short-term instruments such as liquid mutual funds.

Liquid funds invest in money market instruments with maturities of up to 91 days, including:

Treasury Bills

Commercial Papers

Certificates of Deposit

Short-term government securities

Because these instruments mature quickly, liquid funds are commonly used for short-term liquidity management.

In a HYSA structure, the returns generated by these instruments are linked to the user’s spending balance.

How Multipl’s Higher-Yield Spending Account Works

Multipl’s platform integrates liquid mutual funds into a spending-focused account.

Here is the simplified flow.

Step 1: Add Money

Users transfer funds to their Higher-Yield Spending Account through the Multipl app.

Step 2: Allocation to Liquid Mutual Funds

The funds are allocated to liquid mutual funds, which generate returns based on short-term interest rates.

Step 3: Earn While You Wait

While the money sits in the account waiting to be used, it may generate returns linked to the underlying liquid fund performance.

Step 4: Spend or Withdraw Anytime

Users can:

• redeem instantly through brand vouchers

• withdraw funds back to their bank account

• use the money for planned spending goals

The structure is designed to keep the money accessible while still earning.

HYSA vs Savings Account vs Liquid Mutual Fund

Feature | Savings Account | Liquid Mutual Fund | Higher-Yield Spending Account (HYSA) |

|---|---|---|---|

Primary purpose | Daily banking and transactions | Parking short-term surplus cash | Managing spending money more efficiently |

Typical return profile | Usually lower bank interest | Market-linked | Market-linked through liquid funds |

Liquidity | Instant | Usually quick redemption, subject to cut-off/process | Designed for spending and withdrawal access |

Lock-in | None | None | None |

Risk level | Relatively low as bank deposit | Low-risk category, but market-linked | Depends on the underlying liquid fund |

Best use case | Salary credits, ATM use, bill payments | Short-term idle cash | Everyday money waiting to be spent |

Underlying asset | Bank deposits | Money market instruments | Liquid mutual funds wrapped in a spending interface |

Savings accounts prioritise transaction convenience.

Liquid funds are used for short-term cash management.

HYSA tries to combine the return potential of liquid funds with a practical spending workflow.

HYSA vs Liquid Mutual Funds

It also helps to understand how HYSA differs from directly investing in liquid funds.

Feature | Liquid Mutual Fund | HYSA |

|---|---|---|

Primary Purpose | Investment product | Spending-focused account |

Interface | Investment platform | Spending + redemption interface |

Usage | Parking idle cash | Everyday spending money |

Integration | Portfolio-based | Spending workflow |

HYSA basically wraps liquid funds inside a spending interface, making them easier to use for day-to-day money management.

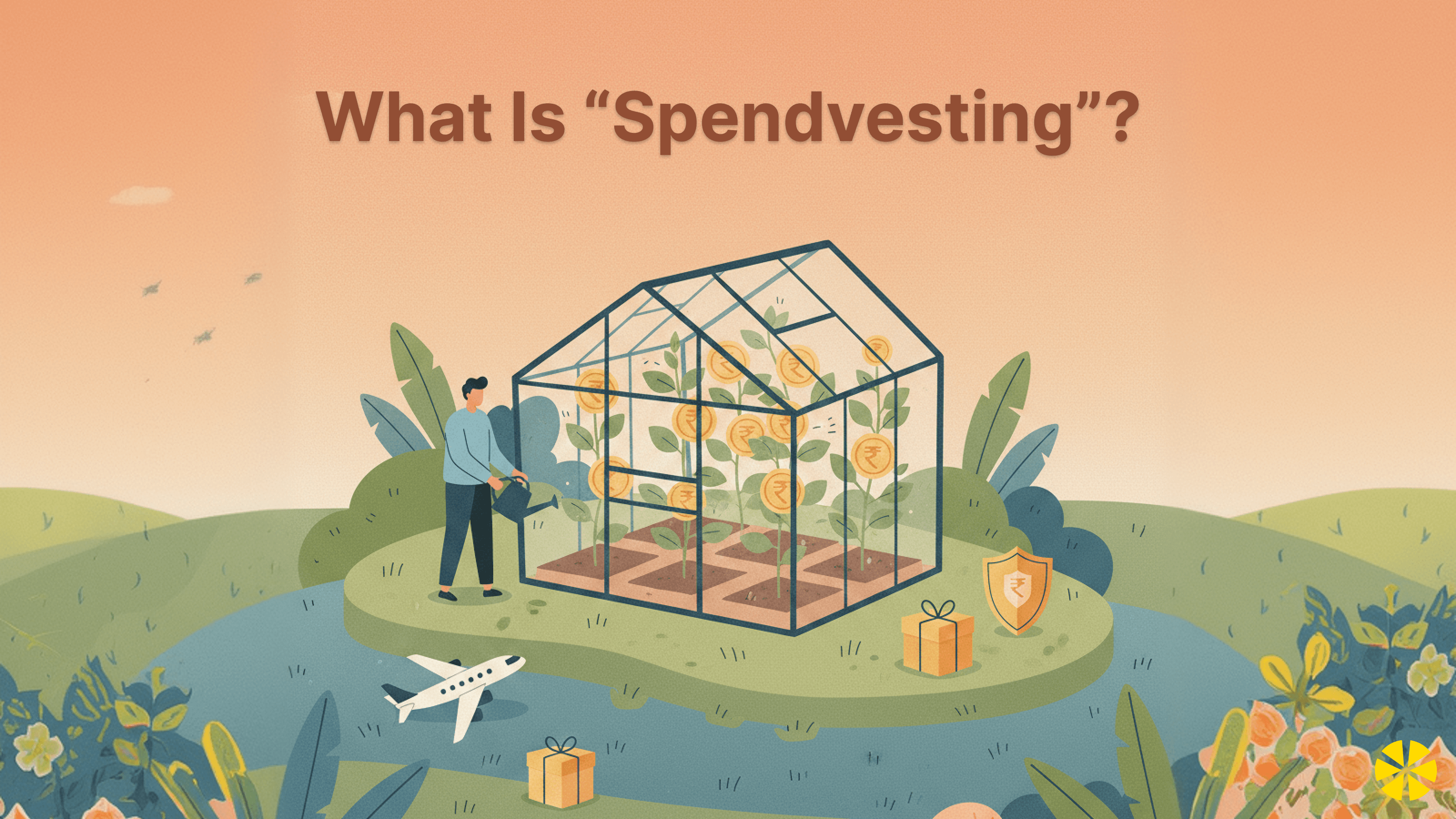

What Is “Spendvesting”?

Multipl often describes this approach as Spendvesting.

Spendvesting means money meant for spending can still keep earning until it is actually used.

Instead of separating spending and investing completely, the two are connected.

For example:

saving for travel

planning a gift purchase

setting aside money for insurance premiums

In these cases, money may wait for weeks or months before it is spent. Spendvesting is about making that waiting period work better.

Think of money waiting for a Swiggy-heavy month, Zepto orders before a party, Uber rides for the week, flight bookings, an iPhone purchase, school fees, or even wedding expenses. If that money is going to be spent soon, many users want it to stay liquid and still earn up to 7% through liquid funds* until they use it.

Who Should Use a Higher-Yield Spending Account?

HYSA structures are usually useful for people who:

receive a monthly salary

keep a balance in their savings account throughout the month

want better use of idle cash

prefer liquidity without lock-in

This is not for long-term investing. It is for short-term spending balances and Planned Spends.

When a Savings Account Still Makes Sense

Savings accounts still matter.

They remain ideal for:

salary deposits

ATM withdrawals

immediate transactions

Many users keep both:

a savings account for transactions

a HYSA for idle spending money

That split can be practical. Keep instant-access banking money in the bank, and move planned spends into a high-yield spending account if you want the money to stay available and earn up to 7%* through low-risk liquid funds.

Frequently Asked Questions

What is HYSA in India?

A Higher-Yield Spending Account (HYSA) is a fintech product that allows everyday spending money to earn returns linked to liquid mutual funds while remaining accessible without lock-in.

Is Multipl the first HYSA platform in India?

Multipl introduced the Higher-Yield Spending Account concept in India by integrating liquid mutual funds with a spending interface designed for everyday money management.

How much can you earn in a HYSA?

Returns are linked to liquid mutual fund performance. Liquid funds have historically often delivered more than standard savings account interest rates, but returns vary with market conditions and are not guaranteed. On Multipl, the framing is up to 7%* based on historical returns of the Liquid Fund category.

Is HYSA safe for emergency funds or monthly expenses?

HYSA can work for short-term cash and planned monthly expenses, but because the underlying product is usually a market-linked liquid mutual fund, it is not the same as keeping money in a bank savings account. Some users may prefer to split money between both, depending on their liquidity needs and risk comfort. No investment is zero-risk.

Is there any lock-in period in a Higher-Yield Spending Account?

Typically, no. HYSA products are designed for accessible short-term money, so users can generally withdraw or redeem without a lock-in period, though redemption timelines can depend on the platform and underlying fund process.

Is a HYSA better than a savings account?

That depends on the use case. If the goal is daily banking, a savings account is still essential. If the goal is to make idle spending money work harder before it gets used, HYSA may be a better fit for that purpose.

Final Thoughts

Most personal finance advice has focused on long-term investing.

But there is another everyday question.

Where should your spending money wait?

Savings accounts have handled that job for decades. Now, fintech products like the Higher-Yield Spending Account are trying to rethink how short-term money is managed.

For Spendvestors, the appeal is simple: liquidity first, no lock-in, access when needed, low-risk liquid funds, and the chance to earn up to 7%* while money waits for real expenses.

And in India, that category begins with Multipl.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633). *Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.