•

1 min read

Short-Term Investment Options in India: 8 Safe Places for Idle Money

TL;DR

The best short-term investment is not the one with the highest return — it’s the one that matches when you need your money and how quickly you need access.

Need money anytime → Savings / Higher-Yield Spending setups

Need it within days → Liquid funds

Can lock for months → FDs, T-bills

The Mistake Most People Make

When people look for short-term investment options in India, they start with:

“Which option gives the highest return?”

That’s the wrong question.

Short-term money is not about maximizing returns.

It’s about not losing flexibility while earning something better than idle cash.

Here’s the better way to think about it:

- Start with time horizon + access needs

- Then choose the product

Step 1: Decide Based on When You Need the Money

Category 1: Need Money Anytime (0–7 days)

This is your active money:

Monthly expenses

Bills

Emergency buffer

Money between salary and spending

Best Options:

Savings Account

Higher-Yield Spending setups (built on liquid funds)

Category 2: Need Money Within Days (7–30 days)

This is waiting money:

Upcoming travel

Insurance premiums

Rent reserves

Best Options:

Liquid Mutual Funds

Overnight Funds

Category 3: Can Lock for 3–12 Months

This is predictable money:

Known future expenses

Short-term savings goals

Best Options:

Fixed Deposits (FDs)

Treasury Bills (T-Bills)

Ultra Short Duration Funds

The 8 Best Short-Term Investment Options in India

Let’s break them down properly.

1. Savings Account

Best for: Daily use, instant access

Liquidity: Instant

Returns: ~2.5–4%

Risk: Very low

Tax: Fully taxable

Reality:

Safe, but inefficient for idle money.

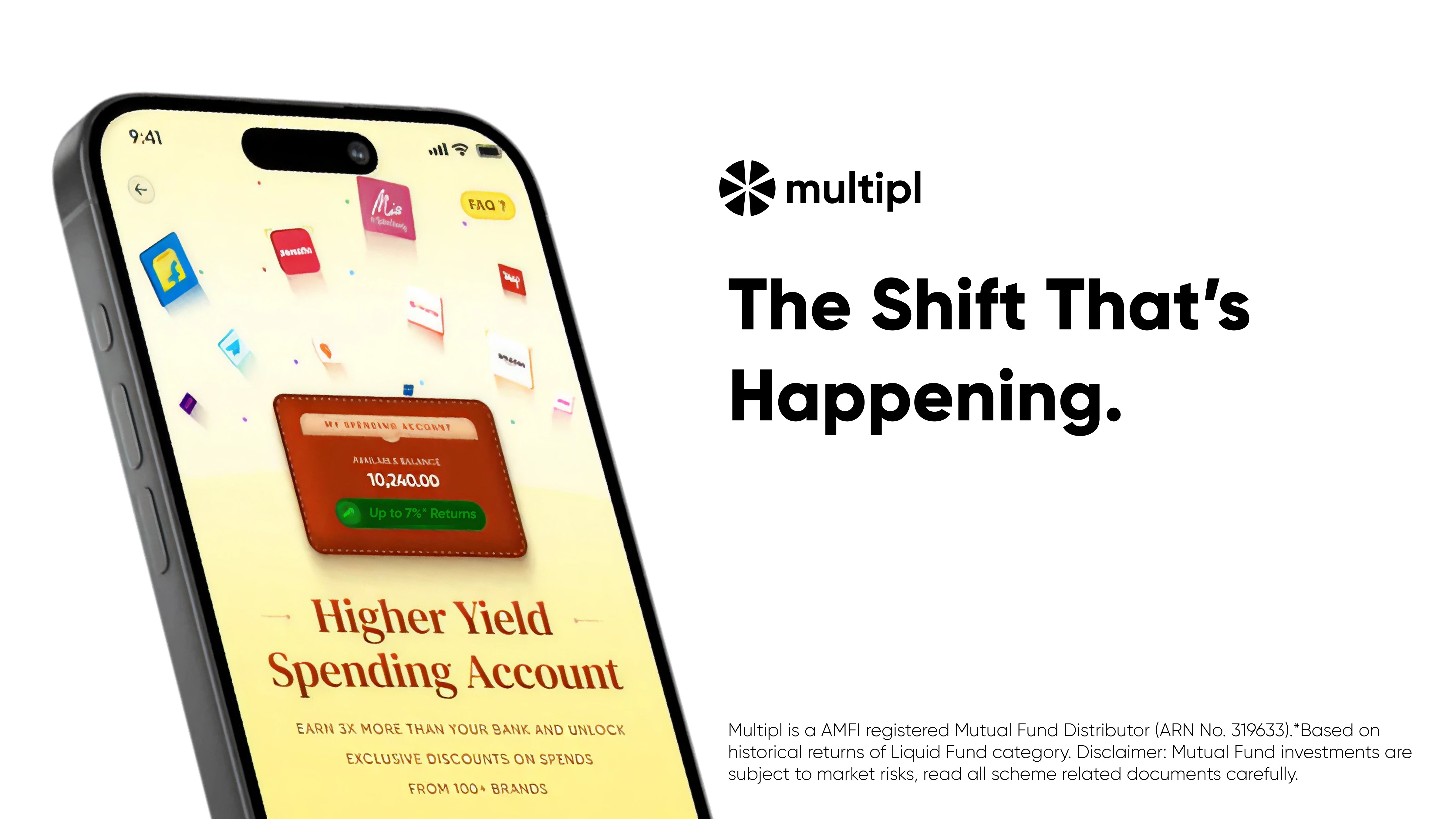

2. Higher-Yield Spending Account

Best for: Everyday money that is waiting to be spent

Liquidity: Instant / near-instant

Returns: Linked to liquid funds (~6–7% historically)

Risk: Low (market-linked)

Tax: As per debt funds

What it solves:

Keeps spending money productive without changing behaviour.

3. Liquid Mutual Funds

Best for: Short-term parking (days to months)

Liquidity: T+1 (often faster depending on platform)

Returns: ~6–7% historically

Risk: Low

Instruments: Treasury bills, CPs, CDs

Key advantage:

Better efficiency than savings accounts without locking money.

4. Overnight Funds

Best for: Ultra-short holding periods (1–3 days)

Liquidity: T+1

Returns: Slightly lower than liquid funds

Risk: Very low

Used for extremely short parking durations.

5. Fixed Deposits (FDs)

Best for: Known timelines with no need for liquidity

Liquidity: Locked (penalty on early withdrawal)

Returns: ~5–7%

Risk: Low

Tax: Fully taxable

Downside:

Penalty kills flexibility.

6. Sweep-in Fixed Deposits

Best for: Bank users wanting auto-optimization

Liquidity: Linked to savings account

Returns: FD-like

Risk: Low

Reality:

Convenient, but still bank-centric and less flexible than funds.

7. Treasury Bills (T-Bills)

Best for: Low-risk investors comfortable with direct instruments

Liquidity: Medium

Returns: Market-driven

Risk: Sovereign-backed

Used more by experienced investors.

8. Ultra Short Duration Funds

Best for: Slightly longer short-term horizons (3–6 months)

Liquidity: High

Returns: Slightly higher than liquid funds

Risk: Moderate (vs liquid funds)

Slightly more volatility than liquid funds.

Quick Comparison Table

Option | Liquidity | Risk | Returns | Best Use Case |

Savings Account | Instant | Very Low | 2.5–4% | Daily transactions |

Higher-Yield Spending | Instant | Low | ~6–7%* | Spending money |

Liquid Funds | T+1 | Low | ~6–7%* | Short-term parking |

Overnight Funds | T+1 | Very Low | Lower | Ultra-short parking |

FD | Locked | Low | 5–7% | Fixed timelines |

Sweep FD | Medium | Low | 5–7% | Passive users |

T-Bills | Medium | Very Low | Market-linked | Advanced users |

Ultra Short Funds | High | Moderate | Slightly higher | 3–6 month horizon |

*Based on historical performance, not guaranteed.

Liquid Funds vs FD vs Savings: What Actually Matters

Most comparisons focus on returns.

But in real life, these factors matter more:

Can you access money when needed?

Will you pay a penalty to exit?

Does it match your timeline?

What happens after tax?

That’s why liquid funds sit in a unique position:

They are:

More flexible than FDs

More efficient than savings accounts

Where Most People Go Wrong

❌ Keeping everything in savings accounts

Mixes spending, emergency, and investment money.

❌ Using FDs for short-term money

Locks money unnecessarily.

❌ Ignoring idle cash

Money sits for weeks/months doing nothing.

A Simpler Way to Decide

Use this:

Need money today? → Savings / Spending account

Need money soon? → Liquid funds

Can lock it? → FD or T-Bills

That’s it.

The Shift That’s Happening

Earlier, you had only:

Savings accounts

Fixed deposits

Now you have:

Liquid funds

Higher-yield spending setups

Which means:

Your money doesn’t have to sit idle anymore

It can stay accessible and productive

Final Thought

Most people focus on how to invest.

Very few think about where their money sits before it gets invested or spent.

But that’s where a surprising amount of money leaks happen.

If your money is waiting, it should be working.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633). *Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.