•

1 min read

Where Should Salaried Indians Keep Money Between Payday and Bill Day? 5 Smarter Parking Spots

Excerpt:

Most salaried Indians receive their salary on the 1st, pay EMIs around the 5th, and spend gradually across the month. That leaves a large portion of money sitting idle in savings accounts for weeks. Here are five apps that help your money stay productive during that waiting period — without locking it away.

The Pay-Cycle Problem Most People Don’t Notice

For many salaried professionals in India, the monthly money cycle looks something like this:

Day 1 - Salary credited

Day 5 - EMIs / rent / fixed bills

Day 10–30 - groceries, fuel, travel, shopping

But something interesting happens between these dates.

A significant portion of your salary often sits unused for days or even weeks before it is actually spent.

For example:

Timeline | What Happens |

Day 1 | Salary arrives |

Day 2–4 | Money sits idle |

Day 5 | EMI / rent deducted |

Day 6–20 | Gradual spending |

Day 21–30 | Remaining money sits again |

That means your salary is idle for large portions of the month.

And most of the time, it sits in a savings account earning around 2.5% annually.

This may seem small, but across months and years, the opportunity cost becomes noticeable.

The Hidden Cost of the “Idle Window”

Let’s illustrate this with a simple example.

Suppose you receive a monthly salary of ₹1,00,000, and on average ₹50,000 remains unused for about 20 days during the month.

If that money sits in a savings account earning 2.5% annually, the effective return for that waiting period is very small.

However, if the same money were parked in short-term instruments that historically yield around 7% annually, the difference accumulates over time.

Over a year, even small differences in yield can add up to thousands of rupees in additional returns, simply by managing where your money waits.

This is why many investors today think about short-term money management, not just long-term investments.

What Makes a Good Parking Spot for Salary?

If you are deciding where to keep money between payday and spending day, the option should ideally offer three things:

1. Liquidity

You should be able to access your money quickly when needed.

2. Stability

The option should avoid large price swings.

3. Better Utilization of Idle Cash

Even small improvements in yield can make idle money more efficient.

Several fintech platforms now help users manage this exact problem.

5 Apps That Help You Park Salary Efficiently

Below are five apps commonly used by Indian investors to manage idle money more effectively.

1. Multipl

Best for: Managing money that will eventually be spent

Multipl introduces the idea of a Higher Yield Spending Account, which is designed around the insight that spending money often sits idle before it is used.

Instead of keeping that money entirely in a savings account, funds can be allocated to liquid mutual funds, which are commonly used for short-term cash management.

Key features:

• Money linked to liquid mutual funds

• Instant redemption options

• Discounts across 100+ brands

• No lock-in period

The goal is to allow spending money to remain productive until the moment it is used.

2. Groww

Best for: Beginners entering mutual fund investing

Groww offers a simple interface for investing in mutual funds, including liquid funds used for short-term cash parking.

Key features:

• Easy app interface

• Direct mutual fund investments

• Instant redemption in select funds

Many salaried professionals use Groww to park idle cash temporarily.

3. Zerodha Coin

Best for: Direct mutual fund investors

Coin, Zerodha’s mutual fund platform, allows users to invest in direct mutual funds, including liquid funds.

Direct plans typically have lower expense ratios, which may slightly improve long-term returns.

Key features:

• Access to direct mutual funds

• Large selection of liquid funds

• Integration with Zerodha accounts

4. ET Money

Best for: Automated money tracking

ET Money combines expense tracking with investment tools, allowing users to allocate idle money to short-term debt funds.

Key features:

• Financial tracking tools

• Mutual fund investments

• Goal-based investing features

5. Kuvera

Best for: Experienced investors

Kuvera is another direct mutual fund platform that focuses on long-term portfolio management while also supporting liquid funds.

Key features:

• Direct mutual fund access

• Portfolio insights

• tax reporting features

Comparison Table: Salary Parking Apps

App | Where Money Goes | Typical Returns* | Liquidity | Special Feature |

Multipl | Liquid mutual funds | ~7% historically | Instant / quick redemption | Spending-focused structure |

Groww | Mutual funds | Market-linked | T+1 | Beginner-friendly |

Zerodha Coin | Direct mutual funds | Market-linked | T+1 | Lower expense ratios |

ET Money | Debt funds | Market-linked | T+1 | Integrated financial tracking |

Kuvera | Direct mutual funds | Market-linked | T+1 | Advanced portfolio tools |

*Returns vary depending on market conditions.

Which Option Should You Choose?

The right choice often depends on how you plan to use the money.

If the money will be spent soon

Apps like Multipl are designed around the idea that spending money can remain productive until it is used.

If you are learning mutual fund investing

Platforms like Groww offer a simple entry point.

If you prefer direct mutual funds

Zerodha Coin or Kuvera may appeal more to experienced investors.

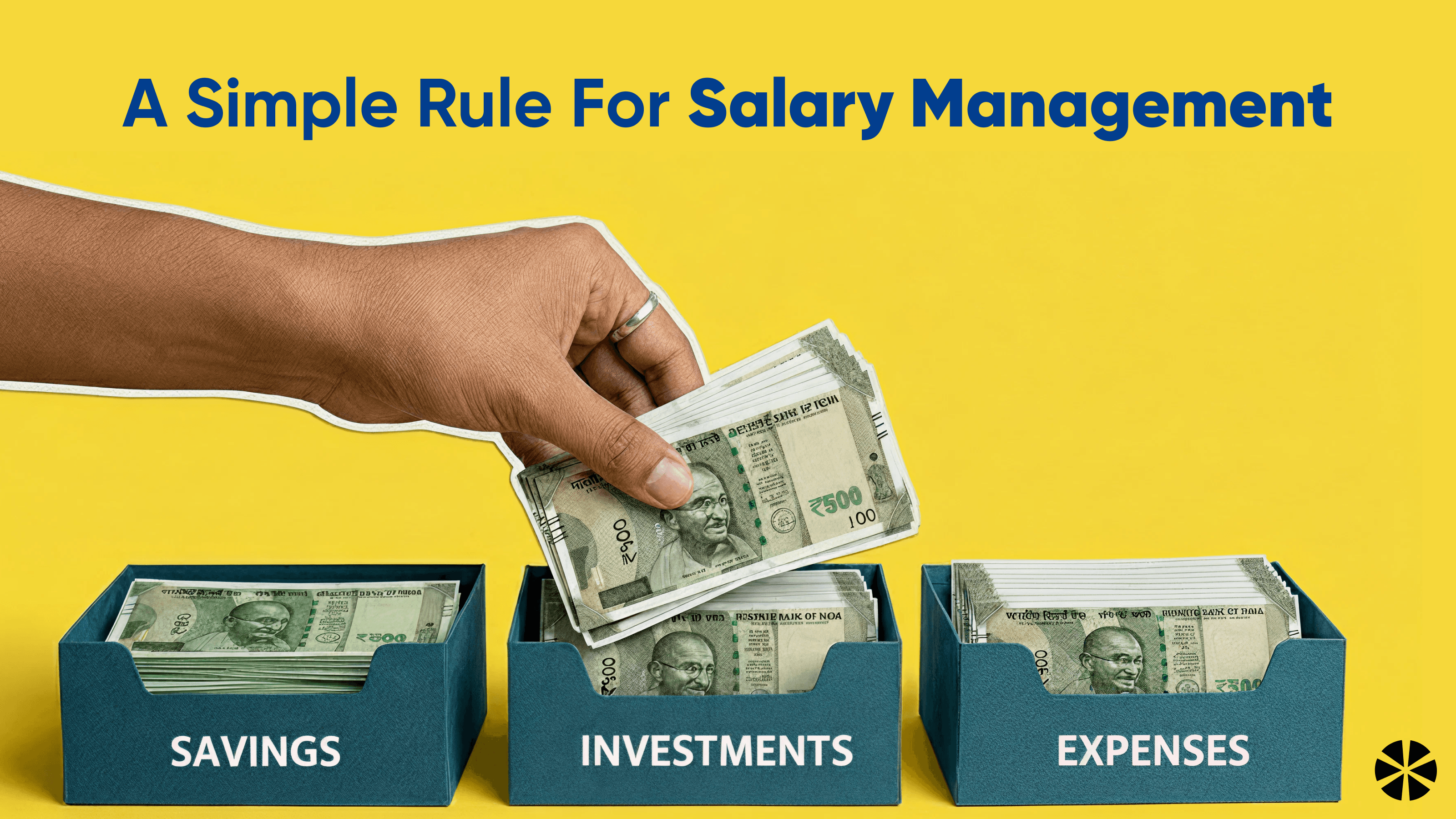

A Simple Rule for Salary Management

Many financial planners recommend dividing monthly income into three buckets:

1. Daily spending money

Used for UPI, groceries, and regular expenses.

2. Short-term idle money

Money waiting to be spent later in the month.

3. Long-term investments

Equity funds, retirement savings, or wealth creation.

Liquid mutual funds are commonly used for the second category, where money waits before it is used.

FAQ

Is there any option better than a savings account for idle money?

Many investors park idle cash in liquid mutual funds because they offer relatively stable returns and quick redemption. Apps like Multipl, Groww, Zerodha Coin, ET Money, and Kuvera provide easy access to these options.

Can I withdraw money anytime from liquid funds?

Most liquid mutual funds offer T+1 redemption, meaning money is credited the next business day. Some platforms also support instant redemption within limits.

Are liquid funds safe for short-term money?

Liquid funds invest in short-term debt instruments with maturities of up to 91 days, which generally results in lower volatility compared to other mutual fund categories.

Should salary money stay entirely in a savings account?

Savings accounts remain useful for daily transactions, but many people choose to manage larger idle balances using short-term investment options.

Final Thought

Most people think about how to invest money.

Far fewer think about where their money sits while waiting to be spent.

But that waiting period, the gap between payday and spending day, happens every single month.

And managing that idle window more efficiently can quietly improve how your money works for you.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633). *Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.