•

1 min read

Liquid Fund Alternatives: What to Pick When It’s Not a Fit

Liquid funds are often the first recommendation when someone wants a smarter place for idle money. And for good reason: they are built for short-term parking, aim to offer relatively easy access, and usually sit lower on the risk spectrum than longer-duration debt funds.

But here’s the part many guides skip: liquid funds are not automatically the best fit for every type of short-term money.

Sometimes you need same-day certainty. Sometimes you care more about capital stability than slightly higher returns. Sometimes you need a guaranteed rate, not a market-linked one. And sometimes the right answer is not a liquid fund at all, but an overnight fund, money market fund, savings account, HYSA-style setup, or even a fixed deposit.

That is what this guide is about.

If you are comparing liquid fund alternatives, this post will help you answer one practical question: where should you park money besides liquid funds, based on when you need it, how much fluctuation you can tolerate, and what kind of access matters most?

If you are new to how liquid funds work, you may want to first read Liquid Mutual Fund Meaning: How It Works in India. If your broader question is whether parked money should stay in a bank or move elsewhere, Idle Cash Strategy: Savings Account or Liquid Fund? is a useful companion piece.

Why liquid funds may not always be the right fit

Liquid funds are debt mutual funds that typically invest in instruments with residual maturity of up to 91 days, as defined in mutual fund categorisation guidance published by AMFI. Overnight funds sit even shorter, while money market funds and ultra-short duration funds extend further out on the maturity and risk-access spectrum. AMFI’s classification page gives the official high-level framework.

That makes liquid funds suitable for many goals, but not all. Here are the common situations where people start looking for alternatives to liquid funds:

1. You need lower NAV movement than a liquid fund can offer

Liquid funds are low risk, but they are not risk-free. Their NAV can move, and although the movement is usually limited compared with longer-duration debt funds, some investors simply want the shortest possible interest-rate and credit exposure. In that case, an overnight fund may feel more appropriate. Multipl explains this trade-off well in Liquid Fund Safety: Can Liquid Funds Lose Money?.

2. You need more certainty than market-linked products provide

If the money is meant for a known expense on a known date, and you do not want any market-linked variability, a bank fixed deposit can be easier to plan around. Guaranteed returns are a real preference for many savers, even if flexibility is lower.

3. You want instant or near-instant access

Redemption speed matters. Even among low-risk funds, access timelines differ by product, platform, and cut-off time. If you expect to need the money at very short notice, compare access rules before choosing. For a practical breakdown, see Liquid Fund Withdrawal: When Can You Get Your Money? and Instant Redemption Liquid Funds: Best Options and Limits in India.

4. You are parking money for only a few days

When the holding period is extremely short, the small return difference between products matters less than ease, certainty, and transaction convenience. That is where savings accounts, sweep structures, or overnight funds can make more sense than a liquid fund.

5. You are comparing beyond “liquid fund vs savings account”

Most people, once educated on liquid funds, move to the next decision stage: money market fund vs liquid fund, overnight fund alternative, FD or fund, or what is better than liquid funds for short term use cases. That comparison layer is where better money decisions usually happen.

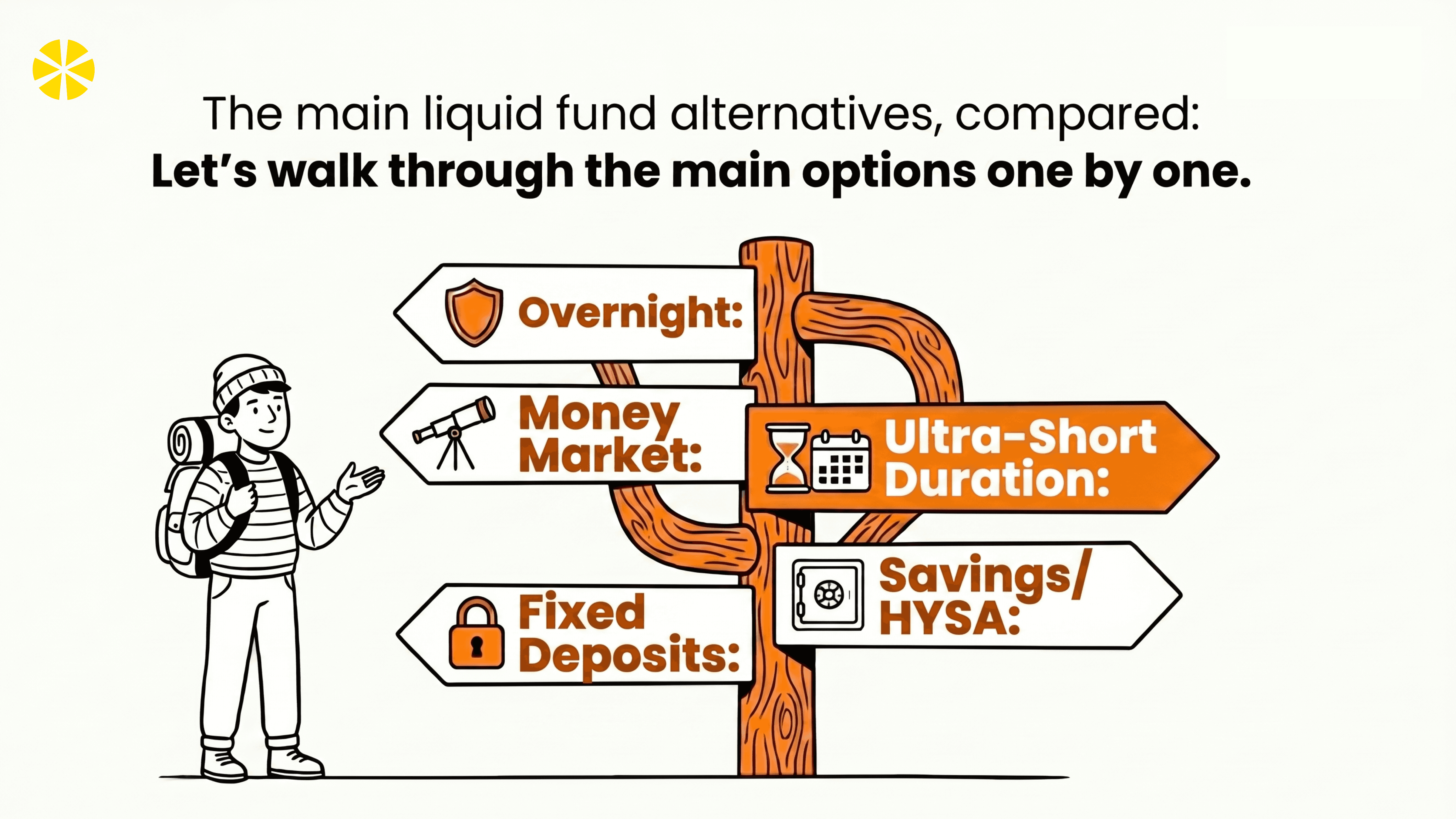

The main liquid fund alternatives, compared

Let’s walk through the main options one by one.

1. Overnight funds: best when stability matters more than yield

If you want the closest mutual-fund alternative to “minimal mark-to-market drama,” overnight funds deserve attention.

Overnight funds invest in securities with a maturity of one day, which materially reduces interest-rate sensitivity compared with liquid funds, according to AMFI’s official scheme categorisation explainer. AMFI’s categorisation guide is a useful reference here.

When an overnight fund is a better fit than a liquid fund

You are holding money for a few days to a few weeks

You want lower NAV volatility

You care more about capital stability than squeezing out extra return

You are parking money before a near-term expense, such as rent, taxes, or a payment milestone

Trade-offs

Expected returns may be slightly lower than liquid funds over some periods

Not all platforms present overnight funds as clearly as liquid funds

Redemption still depends on mutual fund settlement rules, not ATM-style bank liquidity

If you want a side-by-side comparison focused specifically on idle cash products, Liquid Funds vs Overnight Funds: Which Is Better for Idle Cash? goes deeper.

2. Money market funds: best when your horizon is a little longer

A common question is money market fund vs liquid fund. The short answer: money market funds can suit investors willing to hold for a bit longer in exchange for a broader money market opportunity set.

Money market funds invest in money market instruments with maturity up to one year, while liquid funds cap residual maturity at 91 days under the standard classification framework described by AMFI. That longer maturity window can slightly change both return potential and sensitivity profile.

When a money market fund is a better fit

Your parking horizon is a few months, not just a few days

You can tolerate slightly more NAV movement than in a liquid fund

You are optimizing surplus cash beyond immediate emergency access

You are comfortable with debt-fund mechanics and want a step up from pure ultra-short parking

Trade-offs

Less suitable than overnight funds for ultra-short holding periods

Slightly more sensitive to rate movements than liquid funds

Requires more discipline in matching product to time horizon

If you want a broader overview of the category, Exploring Money Market Funds: Stability and Returns helps frame where they fit.

3. Ultra-short duration funds: best for planned short-term surplus, not immediate cash

If you are looking for something potentially better than liquid funds for short term money, ultra-short duration funds may come up. But they are not a direct substitute for emergency liquidity.

These funds usually target a longer portfolio duration than liquid funds, which introduces more scope for NAV movement. That means they may be acceptable for planned short-term surplus, but generally not ideal for money you may need tomorrow.

When they may fit

You know the money can stay put for several months

You are willing to accept somewhat more fluctuation

You are comparing multiple short-term debt buckets, not pure cash parking tools

Trade-offs

More rate sensitivity than liquid or overnight funds

Can disappoint if used like a savings account replacement

Requires more careful horizon matching

This is why many working professionals should not jump from a savings account straight into “whatever debt fund pays more.” Product fit matters more than headline return.

4. Savings accounts and HYSA-style setups: best for convenience and immediate spending

There is a reason savings accounts remain popular: certainty, liquidity, and simplicity.

Banks in India offer immediate access, simple user experience, and low operational friction. RBI publishes reference information on deposit and term rates and regulates the banking system, which is why many users still keep at least a core transactional buffer in a bank account. RBI’s official portal and its rate snapshots provide the regulatory backdrop for how deposit products function.

When a savings account is a better fit than a liquid fund

You need instant access

The money is for frequent transactions

Convenience matters more than return optimization

You do not want to track cut-off times, redemption windows, or settlement timing

Where a HYSA-style approach fits

A higher-yield spending setup aims to bridge the gap between parked money and planned spending. Instead of letting entire balances sit idle in a low-yield savings account, you keep short-term money in a structure designed for better productivity while maintaining spending intent.

To understand how this works in the Multipl ecosystem, read What Is a Higher-Yield Spending Account (HYSA) and How Does Multipl Work? A Complete 2026 Guide. You can also explore The Spending Money Hack: How to Use HYSA (Higher-Yield Spending account) to Earn While You Shop for a more practical explanation.

Trade-offs

Plain savings accounts usually offer lower return potential than market-linked parked-money options

HYSA-style structures require understanding the product rules and usage flow

Transaction convenience differs by provider

If your question is specifically about where salary or monthly cash should sit between earning and spending, Where Should Salaried Indians Keep Money Between Payday and Bill Day? 5 Smarter Parking Spots is highly relevant.

5. Fixed deposits: best when guaranteed rates matter most

Fixed deposits remain one of the clearest alternatives to liquid funds for conservative savers.

They are easy to understand, offer rate visibility upfront, and can work well when your money has a fixed use date and does not need flexible access. RBI’s published deposit-rate snapshots show that term deposit rates can materially differ from savings deposit rates depending on tenure and prevailing conditions. RBI rate data is a useful official benchmark.

When an FD is a better fit than a liquid fund

You want a guaranteed return, not a variable NAV outcome

Your expense is planned and the money can stay locked for the chosen tenure

You are highly risk-averse

You prefer banking products over mutual fund products

Trade-offs

Lower flexibility if you need to break the deposit

Possible penalty on premature withdrawal

Less efficient for money that moves in and out frequently

For a broader comparison mindset, Mutual Funds vs Fixed Deposits: Where Should You Park Your Money? is a useful next read.

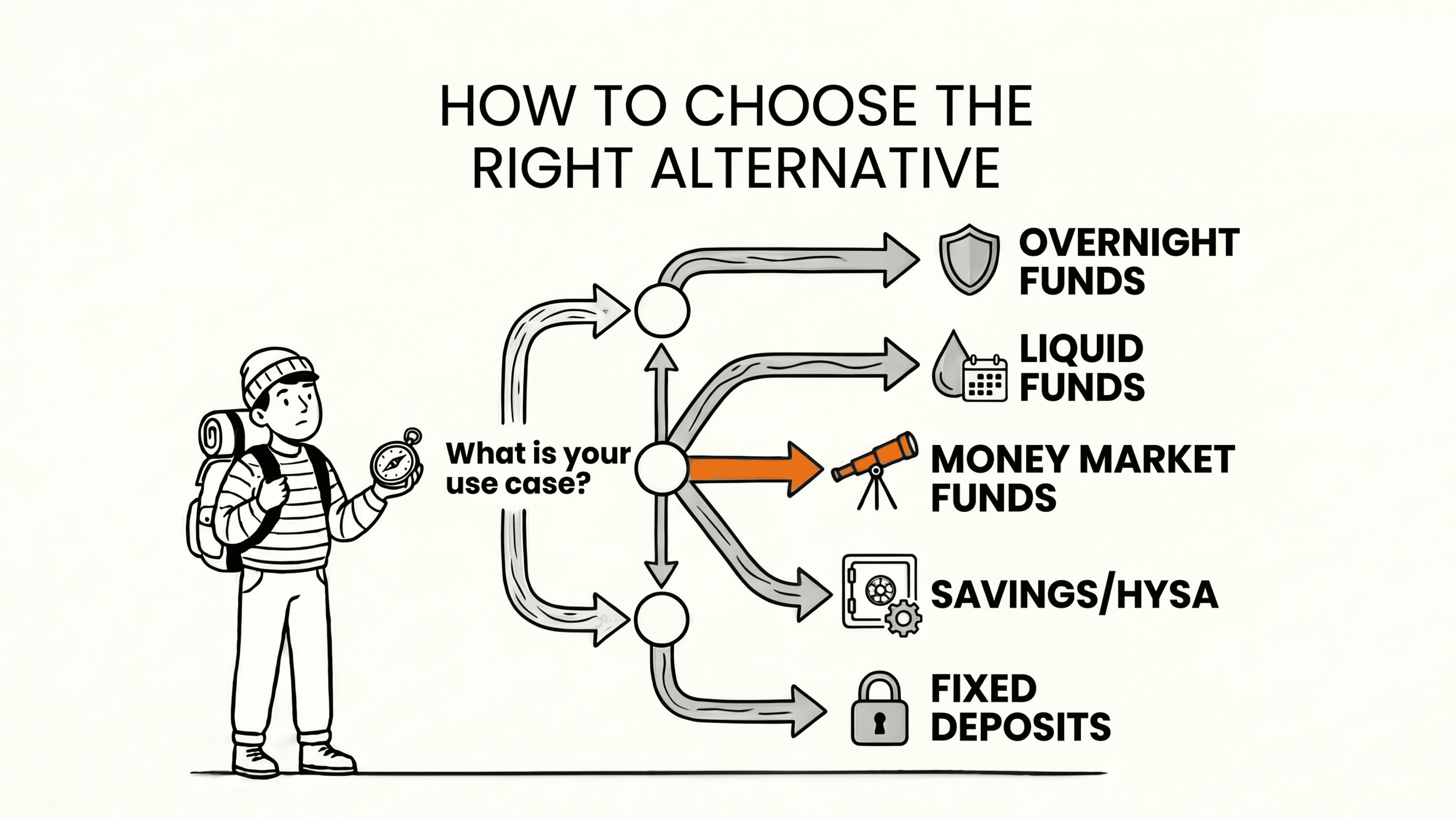

How to choose the right alternative based on use case

The biggest mistake people make is asking, “Which one gives the highest return?”

The better question is: What job does this money need to do?

Here’s a simple framework.

Pick an overnight fund if:

You need a mutual fund option for very short horizons

Capital stability matters more than chasing slightly higher returns

You are uncomfortable with even modest NAV movement in a liquid fund

Pick a liquid fund if:

You want a balance of short-term access and potentially better productivity than idle bank cash

Your horizon is short, but not ultra-immediate

You understand that returns are market-linked, not guaranteed

If you want to assess whether liquid funds are even appropriate for your goal bucket, Liquid Funds for Short-Term Goals: Vacation, Wedding & More can help.

Pick a money market fund if:

You have a somewhat longer surplus horizon

You are comfortable taking a bit more duration exposure than in a liquid fund

You are optimizing planned surplus rather than emergency cash

Pick a savings account or HYSA-style setup if:

The money is part of your active spending cycle

You need quick access and low friction

Convenience and usability matter as much as return

Pick an FD if:

You need certainty

You know the expense date

You value guaranteed rate over flexibility

What “better than liquid funds for short term” really means

The phrase better than liquid funds for short term can be misleading because “better” depends on the constraint.

A product may be better than a liquid fund because it offers:

Lower NAV movement: overnight fund

Higher convenience: savings account

Guaranteed rate: fixed deposit

Broader short-term debt opportunity: money market fund

Better alignment with spending goals: HYSA-style approach

So instead of hunting for one universal winner, map the product to the purpose.

That is also why thoughtful parked-money strategy matters more than just picking a fund category. If you want a broader playbook for short-term cash, The Complete Guide to Managing Short-Term Money in India (2026): Savings Accounts, Liquid Mutual Funds, and Higher-Yield Spending Accounts brings the full framework together.

A practical decision table

Here is the simplest way to think about where to park money besides liquid funds:

If your priority is… | Best-fit option |

|---|---|

Same-day convenience and everyday transactions | Savings account / HYSA-style setup |

Lowest mutual-fund-style volatility for very short periods | Overnight fund |

Balanced short-term parking | Liquid fund |

Slightly longer short-term surplus optimization | Money market fund |

Guaranteed outcome on a known timeline | Fixed deposit |

Notice what is missing: there is no single “best” option.

The right choice depends on whether you care most about:

access,

certainty,

stability,

flexibility,

or return potential.

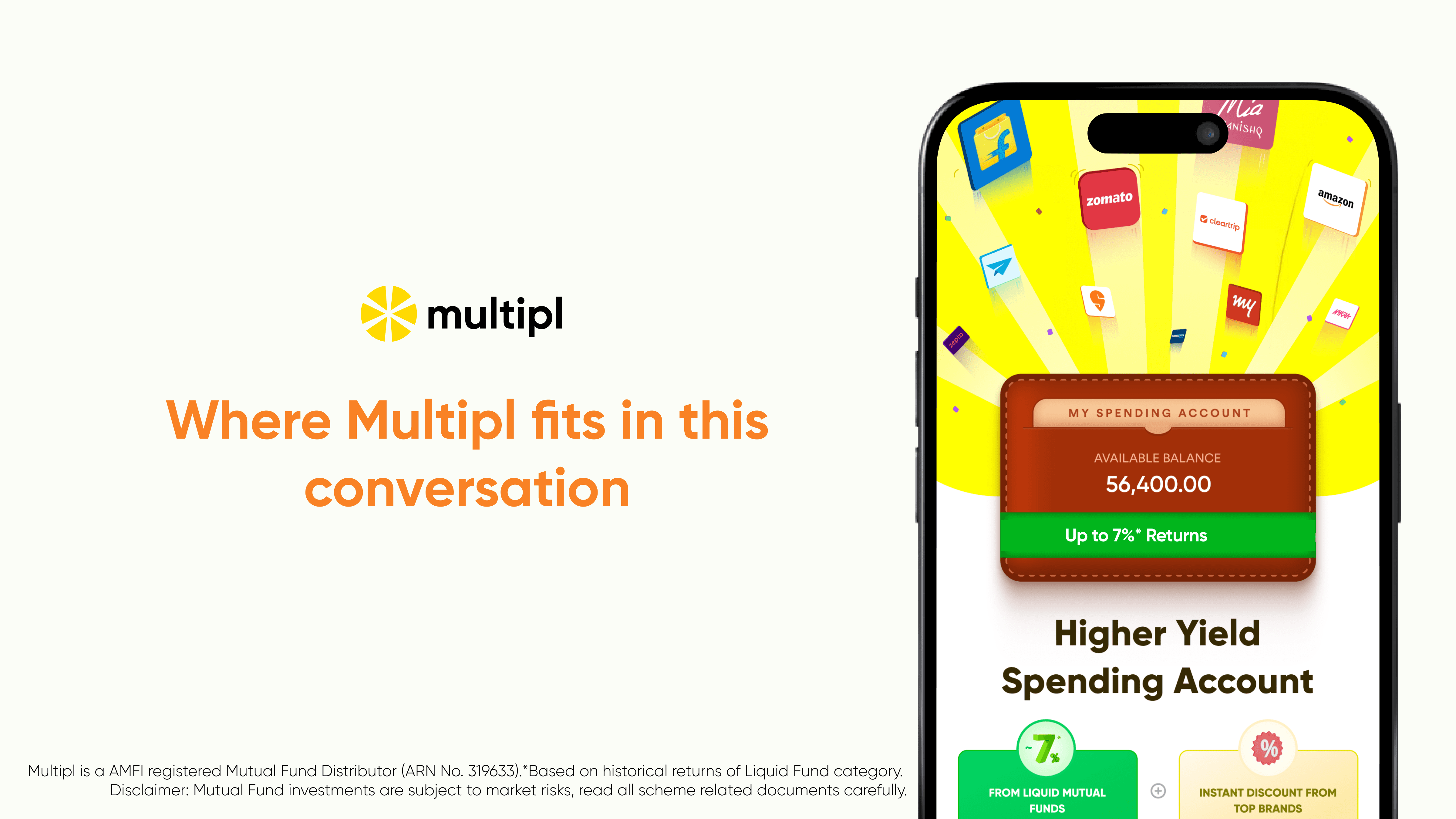

Where Multipl fits in this conversation

Multipl’s positioning is useful for people who do not want their short-term money to remain completely idle, but also do not want to jump blindly into unsuitable products.

Instead of treating all spare cash the same, the smarter approach is to separate money into buckets:

money you may spend soon,

money you need on a planned date,

money that must stay instantly accessible,

and money that can work a bit harder for a defined short-term goal.

That is the core mindset behind spendvesting. If that idea is new to you, What is spendvesting? is the best place to start. And if you want to explore the product side directly, Turn Your Future Expenses into Smart Investments. is the natural next step.

Conclusion

Liquid funds are excellent tools, but they are not the answer to every short-term cash question.

If a liquid fund feels too market-linked, look at overnight funds.

If your horizon is longer and more flexible, consider money market funds.

If convenience matters most, keep the money in a savings account or HYSA-style system.

If certainty is non-negotiable, a fixed deposit may be the better choice.

The smartest savers do not ask, “What is the best product?”

They ask, “What is the best product for this specific money?”

That shift is what turns cash parking from a random decision into a repeatable system.

FAQs

What are the best liquid fund alternatives in India?

The best liquid fund alternatives depend on your need. Overnight funds work well for very short holding periods and lower NAV movement. Money market funds may suit slightly longer surplus cash. Savings accounts or HYSA-style setups fit transactional money. Fixed deposits are better when guaranteed returns matter most.

What is better than a liquid fund for short term money?

If by “better” you mean more stable, an overnight fund may be better. If you mean more convenient, a savings account is better. If you mean guaranteed return, an FD is better. If you mean slightly longer short-term optimization, a money market fund may be a better fit.

Money market fund vs liquid fund: which should I choose?

Choose a liquid fund when your horizon is shorter and you want more conservative cash parking. Choose a money market fund when you can stay invested a little longer and are comfortable with a somewhat broader maturity profile.

Where should I park money besides liquid funds?

The main options are overnight funds, money market funds, ultra-short duration funds, savings accounts, HYSA-style products, and fixed deposits. The right choice depends on how soon you need the money and whether access, safety, or certainty matters most.

Is an overnight fund a good alternative to a liquid fund?

Yes, especially if you want a lower-volatility mutual fund option for money you may need soon. It is often the strongest overnight fund alternative conversation in reverse: when liquid funds feel slightly too flexible on risk, overnight funds become the more conservative pick.

Are liquid funds safer than savings accounts?

They are different products. Savings accounts offer banking convenience and straightforward access, while liquid funds are market-linked mutual funds. Liquid funds are generally low risk, but they do not offer the same kind of certainty as a bank deposit product.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633).

*Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.