•

1 min read

Idle Money in Savings Account: What to Do Instead

TL;DR

If your money is just sitting in a savings account earning ~2.5%, you’re not losing it, you’re just not using it well. The smarter move isn’t “investing harder,” it’s parking idle cash based on when you need it. This guide shows exactly what to do- day by day, week by week.

The Quiet Problem: Idle Money

Most people don’t think twice about this:

Salary gets credited

Money sits in the account

Expenses happen over time

That “sitting” phase?

That’s idle money.

This includes:

Salary waiting to be spent

Emergency buffers

Travel savings

Money for upcoming bills

And almost all of it sits in a savings account by default.

Why Savings Accounts Fall Short

Savings accounts are built for:

Convenience

Transactions

Accessibility

Not for returns.

Typical reality in India:

Savings account: ~2.5%

Inflation: ~5–6%

So your money isn’t really growing meaningfully while it waits.

The Right Way to Think About Idle Money

Instead of asking:

“Where should I invest this?”

Ask:

“When will I need this money?”

That single question changes everything.

The Simple Action Framework (Use This)

Money you need today

Examples:

Daily expenses

UPI transactions

Immediate payments

Where to keep it:

Savings account

No optimization needed. This is working money.

Money you need this week

Examples:

Credit card bill

Rent due in a few days

Where to keep it:

Savings account or near-instant access options

Priority = zero friction

Money you need this month

Examples:

Groceries budget

Monthly lifestyle spend

Subscriptions

Better option:

Higher-yield, liquid setups (built on liquid funds)

Why?

Still accessible

Earns more while waiting

Money you need in 1–6 months

Examples:

Travel fund

Insurance premium

Gadget purchase

Best fit:

Liquid mutual funds

Why?

Historically ~7% range

T+1 access

No lock-in

Money you need after 6+ months

Examples:

Big planned purchases

Medium-term goals

Options:

Short-term debt funds

FDs (if timeline fixed)

What Most People Do (And Why It’s Inefficient)

❌ Keep everything in one savings account

❌ Mix emergency + spending + investment money

❌ Ignore idle cash completely

Result:

Money is safe, but not efficient.

A Simple Example

Let’s say ₹1,00,000 sits in your account for 3 months.

Where it sits | What you earn |

Savings account (2.5%) | ~₹625 |

Liquid fund (~7%) | ~₹1,750 |

Difference: ₹1,125

For doing nothing different.

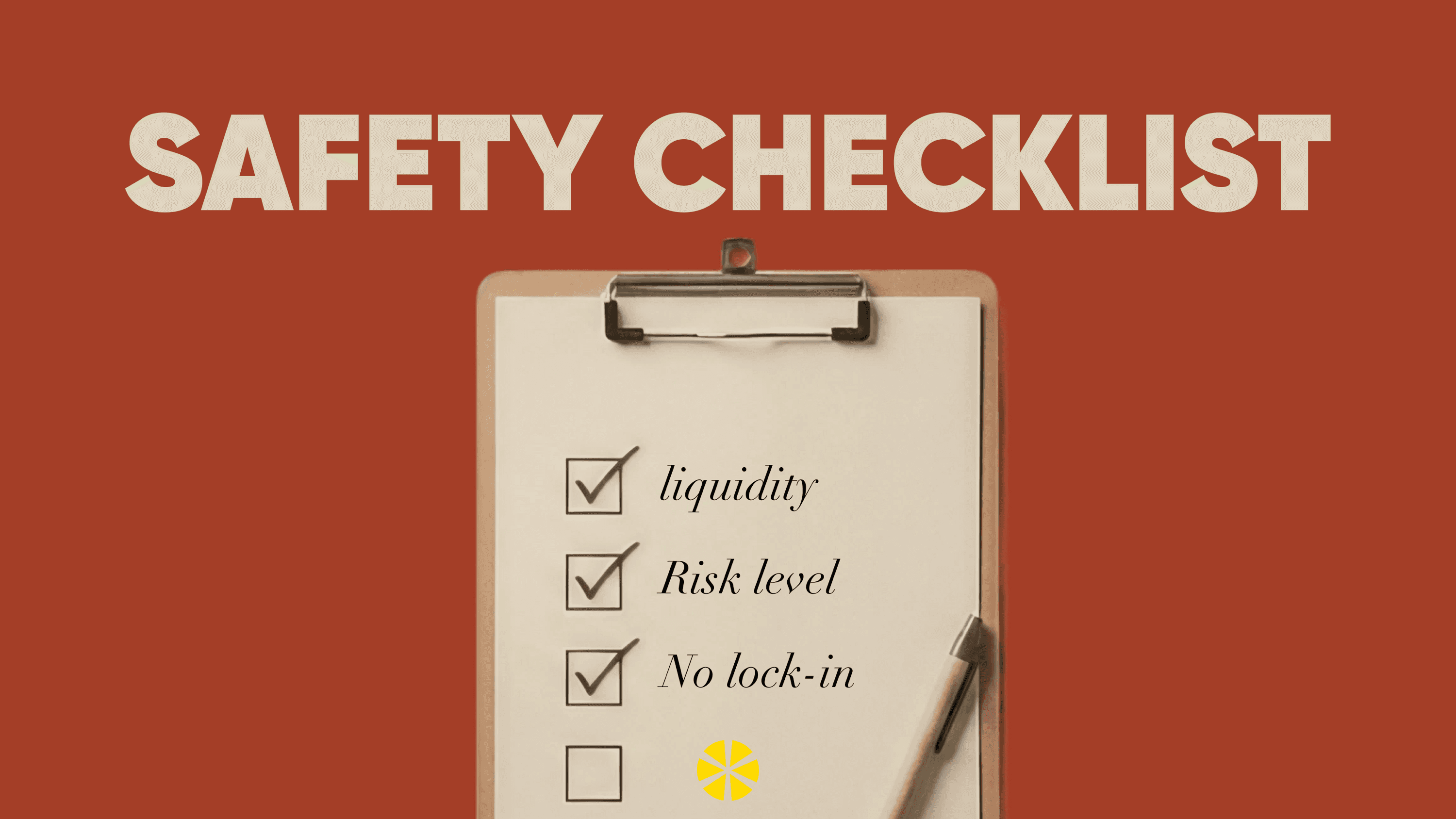

Safety Checklist (Before You Move Money)

If you’re considering alternatives, check:

1. Liquidity

Can you withdraw quickly?

Same day or T+1 is ideal

2. Risk level

Avoid equity for short-term money

Stick to low-risk debt instruments

3. No lock-in

Your money should not be stuck

Avoid unnecessary penalties

4. Simplicity

If it feels complicated, you won’t use it

Ease matters more than optimization

Where Liquid Mutual Funds Fit

Liquid funds are designed for exactly this:

Short-term parking

High liquidity

Low volatility (compared to equities)

They invest in:

Treasury bills

Government securities

High-quality short-term instruments

Think of them as a better waiting room for money

Where Higher-Yield Spending Accounts Fit

Here’s where things get more practical.

Instead of:

Moving money manually

Thinking in “investment steps”

A Higher-Yield Spending Account:

Keeps your spending money accessible

Parks it in liquid funds in the background

Lets it earn while you continue spending normally

Same behavior. Better outcome.

The Real Insight Most People Miss

You don’t need:

Better stock picks

More complex investments

You need:

Better handling of idle money

Because:

A large part of your money is always “in transit”

Not fully spent

Not fully invested

And that’s where efficiency is lost.

Final Thought

Savings accounts aren’t wrong.

They’re just incomplete.

Use them for:

Transactions

Immediate access

But for money that is waiting:

Give it a better place to sit.

Bottom line:You don’t have to change how you spend.You just need to change where your money waits.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633). *Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.