•

1 min read

Higher Yield Spending Account for Everyday Money

TL;DR

A Higher-Yield Spending Account helps your everyday money earn more while staying fully accessible. It’s not a long-term investment product. It’s a smarter place for money that is waiting to be spent.

Your Money Isn’t Just Sitting. It’s Waiting.

Every month, your money follows a pattern:

Salary → waiting → spending → repeat

That “waiting” phase includes:

Monthly expenses

Credit card payments

Travel funds

Insurance premiums

Everyday buffers

Most of this money sits in a savings account earning ~2.5%.

It feels normal.

It’s also inefficient.

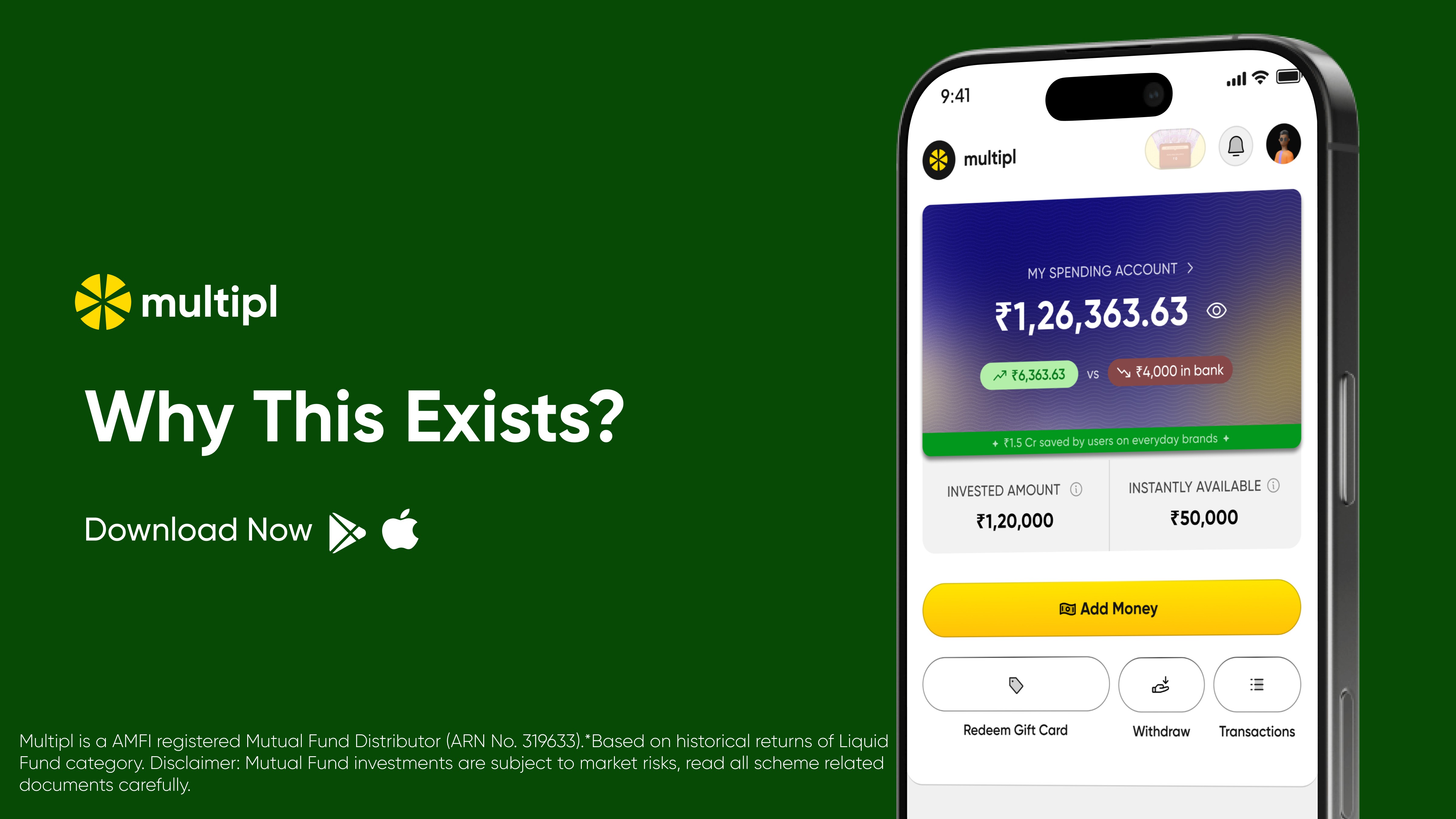

What Is a Higher-Yield Spending Account?

A Higher-Yield Spending Account is designed for:

Money you plan to spend, not invest

It allows you to:

Keep your money accessible

Earn more than a typical savings account

Continue spending normally

Instead of letting your money sit idle, it remains productive while it waits.

How It Works (Plain English)

You add money like you would in any account

That money is allocated to liquid mutual funds

It earns returns based on short-term debt instruments

You can withdraw or spend when needed

No lock-ins.

No long-term commitment.

No change in behavior.

Why This Exists

Savings accounts were built for:

Deposits

Withdrawals

Transactions

Not for maximizing returns.

Liquid mutual funds were built for:

Efficient short-term cash management

A Higher-Yield Spending Account combines both:

Accessibility of a bank account + efficiency of liquid funds

What Makes It Different

1. Built for Spending Money

Not for long-term investing

Not for market speculation

This is for:

Monthly expenses

Bills

Lifestyle spending

2. Better Use of Idle Cash

Instead of:

Sitting at ~2.5%

Your money:

Earns in line with liquid fund returns (historically higher, not guaranteed)

3. No Behavior Change Required

You don’t need to:

Learn investing

Track markets

Time entries and exits

You use it like you already use your money.

4. High Liquidity

Withdraw when needed

Access remains simple

Who Is This For?

Salaried Professionals

Monthly spending buffer

Credit card bill payments

Freelancers

Irregular income cycles

Cash sitting between projects

Planners

Travel funds

Insurance premiums

Upcoming big expenses

Where It Fits (vs Other Options)

Use Case | Best Option |

Daily transactions | Savings account |

Spending money | Higher-Yield Spending Account |

Emergency fund | Liquid mutual funds |

Long-term goals | Equity / investment products |

Why Not Just Use a Savings Account?

Because:

It prioritizes convenience over efficiency

Returns are low (~2.5%)

Large portions of money remain idle

It’s not wrong.

It’s just incomplete.

Why Not Just Use a Mutual Fund App?

Because:

You have to manually invest and redeem

It feels like an “investment decision”

Not built for daily money movement

A Higher-Yield Spending Account removes that friction.

Why Not Use Sweep Accounts or FDs?

Sweep accounts:

Lower returns than optimized options

Bank-controlled structure

FDs:

Lock-ins

Not flexible for spending money

Trust & Safety

Your money is:

Invested in SEBI-regulated liquid mutual funds

Managed by established Asset Management Companies (AMCs)

Held in your name

Liquid funds typically invest in:

Government securities

Treasury bills

High-quality short-term instruments

Common Questions

Is this safe?

Liquid mutual funds are considered lower risk compared to equity funds. However, returns are market-linked and not guaranteed.

Can I withdraw anytime?

Yes. Liquidity is designed to remain high, though timelines may depend on processing structures.

Is there a lock-in?

No lock-in period.

Is this a replacement for a savings account?

No.

Use savings accounts for daily transactions.

Use this for money that is waiting to be spent.

Do I need to understand investing?

No. This is designed to work in the background.

The Bigger Shift

Earlier, you had two choices:

Savings account

Fixed deposits

Now, money doesn’t have to be static.

It can be:

Accessible

Flexible

Productive

At the same time.

Final Thought

Most people try to improve their finances by:

Investing more

Cutting expenses

But one of the simplest upgrades is this:

Stop letting your everyday money sit idle

Start Smarter Cash Management

If your money is going to be spent anyway, the real question is:

Should it sit at ~2.5%… or earn more while it waits?

Explore a Higher-Yield Spending Account and upgrade where your money sits.

Multipl is a AMFI registered Mutual Fund Distributor (ARN No. 319633). *Based on historical returns of Liquid Fund category.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.